The Flutter Entertainment plc (NYSE:FLUT) share price has fared very poorly over the last month, falling by a substantial 26%. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 38% share price drop.

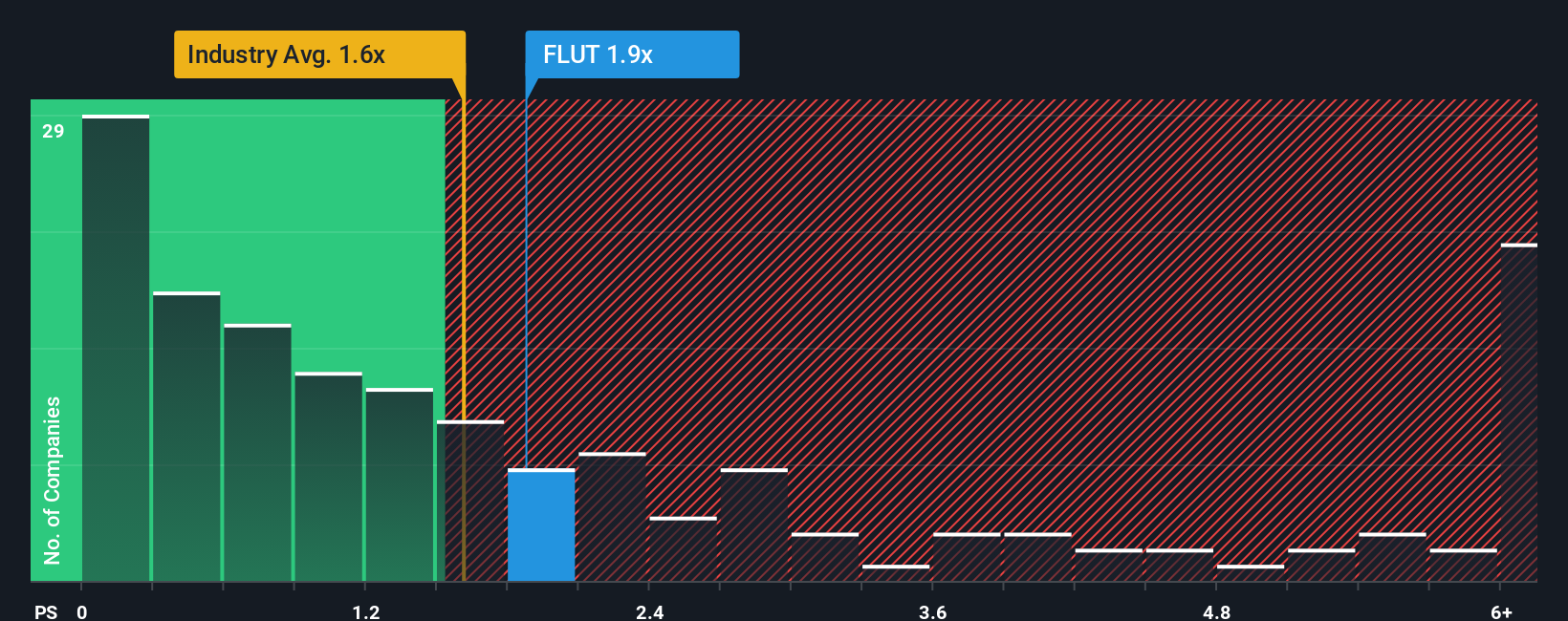

Even after such a large drop in price, you could still be forgiven for feeling indifferent about Flutter Entertainment’s P/S ratio of 1.8x, since the median price-to-sales (or “P/S”) ratio for the Hospitality industry in the United States is also close to 1.6x. Although, it’s not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Flutter Entertainment

How Has Flutter Entertainment Performed Recently?

There hasn’t been much to differentiate Flutter Entertainment’s and the industry’s revenue growth lately. Perhaps the market is expecting future revenue performance to show no drastic signs of changing, justifying the P/S being at current levels. If this is the case, then at least existing shareholders won’t be losing sleep over the current share price.

If you’d like to see what analysts are forecasting going forward, you should check out our free report on Flutter Entertainment.

How Is Flutter Entertainment’s Revenue Growth Trending?

In order to justify its P/S ratio, Flutter Entertainment would need to produce growth that’s similar to the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 14% last year. Pleasingly, revenue has also lifted 57% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 14% each year during the coming three years according to the analysts following the company. With the industry predicted to deliver 14% growth each year, the company is positioned for a comparable revenue result.

With this information, we can see why Flutter Entertainment is trading at a fairly similar P/S to the industry. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Final Word

Flutter Entertainment’s plummeting stock price has brought its P/S back to a similar region as the rest of the industry. While the price-to-sales ratio shouldn’t be the defining factor in whether you buy a stock or not, it’s quite a capable barometer of revenue expectations.

We’ve seen that Flutter Entertainment maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won’t throw up any surprises. All things considered, if the P/S and revenue estimates contain no major shocks, then it’s hard to see the share price moving strongly in either direction in the near future.

Many other vital risk factors can be found on the company’s balance sheet. Take a look at our free balance sheet analysis for Flutter Entertainment with six simple checks on some of these key factors.

If you’re unsure about the strength of Flutter Entertainment’s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’