Warner Music Group (WMG) is back on investors’ radar after its subsidiary WMG Acquisition Corp entered a new multi year credit agreement with JPMorgan Chase, refinancing and consolidating existing debt facilities.

See our latest analysis for Warner Music Group.

That refinancing news lands after a mixed run for investors, with a 1 day share price return of 0.90%, a 30 day share price decline of 8.61%, and a 1 year total shareholder return decline of 17.16%, suggesting momentum has faded recently despite the improved financing flexibility.

If this credit move has you thinking about where else capital could work harder, it might be a good time to scan 20 top founder-led companies as potential long term compounders beyond music and media.

With Warner Music shares down over the past year but trading at a discount to some analyst targets and one valuation estimate, the key question now is whether this is a reset that creates upside or whether the market already reflects future growth.

Most Popular Narrative: 27.8% Undervalued

At a last close of $27.05 versus a widely followed fair value of $37.44, the current Warner Music Group price sits well below that narrative anchor and puts the spotlight on what is driving such a wide gap.

Early adoption of AI-driven analytics and digital marketing tools (e.g., WMG Pulse), combined with an always-on approach to both new releases and catalog marketing, allows Warner to optimize audience targeting and catalog performance, which is expected to drive both scalable revenue growth and operating leverage.

Curious how that sort of AI led catalog engine gets translated into a fair value nearly $10 above today’s price, and what revenue, margin and earnings trajectory that narrative is banking on to justify it, including the profit profile that would need to underpin a higher long term valuation multiple.

Result: Fair Value of $37.44 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the bullish AI and catalog story still runs into real pressure points, including weaker recent cash generation and the execution risk tied to big ticket catalog deals.

Find out about the key risks to this Warner Music Group narrative.

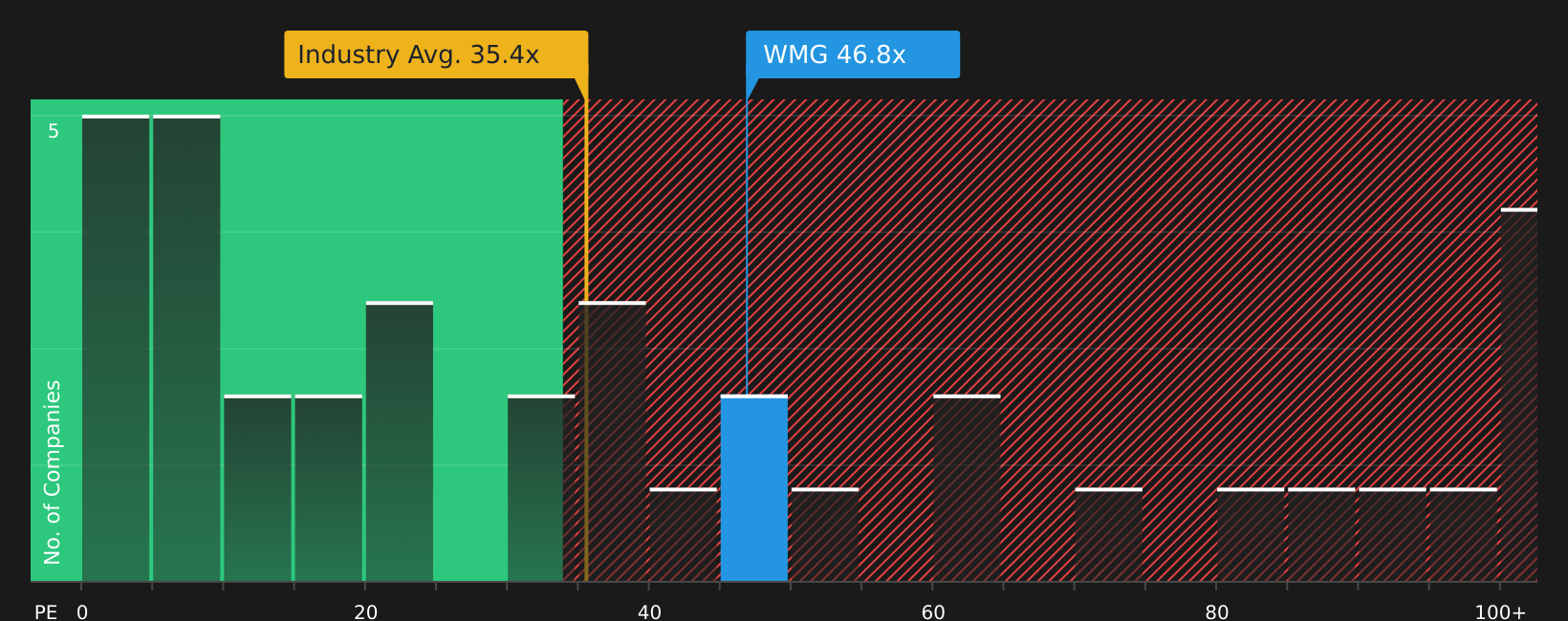

Another View: Earnings Multiple Sends a Different Signal

While the SWS DCF model points to WMG trading about 30.1% below an estimated fair value of $38.72, the current P/E of 46.8x paints a very different picture, looking expensive versus a fair ratio of 35.2x and an industry average of 36.1x. That kind of gap can indicate valuation risk if the story weakens, so investors may need to consider which signal they find more informative at this time.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of opportunity and concern feels familiar, do not sit on the fence. Weigh both sides by checking 3 key rewards and 4 important warning signs today and decide where you stand.

Ready to act on these insights?

You have seen how one stock’s story can split opinion, so do not stop here when a broader watchlist could sharpen your next move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Warner Music Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’

![[L-R] Professor Tshidi Mohapeloa, Dean of Commerce; Professor Michelle Karels, Registrar; Dr Kwezi Mzilikazi, Deputy Vice Chancellor: Research, Innovation and Strategic Partnerships; Professor 'Mabokang Monnapula-Mapesela, Deputy Vice Chancellor: Academic and Student Affairs; Professor Siphokazi Magadla, Dean of Humanities; and Professor Boudina McConnachie, Head of Music and Musicology. [PIC: Micky Oscar]](https://celebrity.land/en/wp-content/uploads/2026/07/Latest-News-Where-language-ends-music-speaks-Professor-Catherine-350x250.png)