Live Nation Entertainment (LYV) is back in focus after recent share price moves, with the stock closing at US$160.32. That puts fresh attention on how its live events, ticketing, and sponsorship business is currently valued.

See our latest analysis for Live Nation Entertainment.

The 7.37% 1 month share price return and 12.00% 3 month share price return suggest momentum has been building, while the 10.33% year to date share price return sits alongside a 1 year total shareholder return of 38.46%.

If Live Nation’s run has caught your eye, you might also want to see which other entertainment related names are gaining attention through our 18 top founder-led companies.

With Live Nation now at US$160.32 and trading at a discount to the average analyst price target of US$183.27, the key question is whether the recent rally still leaves upside or if the market is already pricing in future growth.

Most Popular Narrative: 12.2% Undervalued

Live Nation Entertainment’s most followed narrative points to a fair value of $182.59 per share, compared with the recent close at $160.32. That places this story firmly in the spotlight for anyone tracking the stock’s move.

The experience economy is fueling robust, sustained consumer demand for concerts and festivals worldwide, as evidenced by record ticket sales, growing international fan attendance, and strong sell through rates. This dynamic underpins continued top line expansion and higher on site spending per event, supporting both revenue and margin growth.

Want to see what is baked into that fair value? Revenue expansion, margin lift and a future earnings multiple that assumes a lot has to go right. Curious which assumptions matter most here.

Result: Fair Value of $182.59 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the picture is not one sided, with ongoing antitrust and regulatory scrutiny, as well as potential Ticketmaster growth constraints, both capable of resetting those fair value assumptions.

Find out about the key risks to this Live Nation Entertainment narrative.

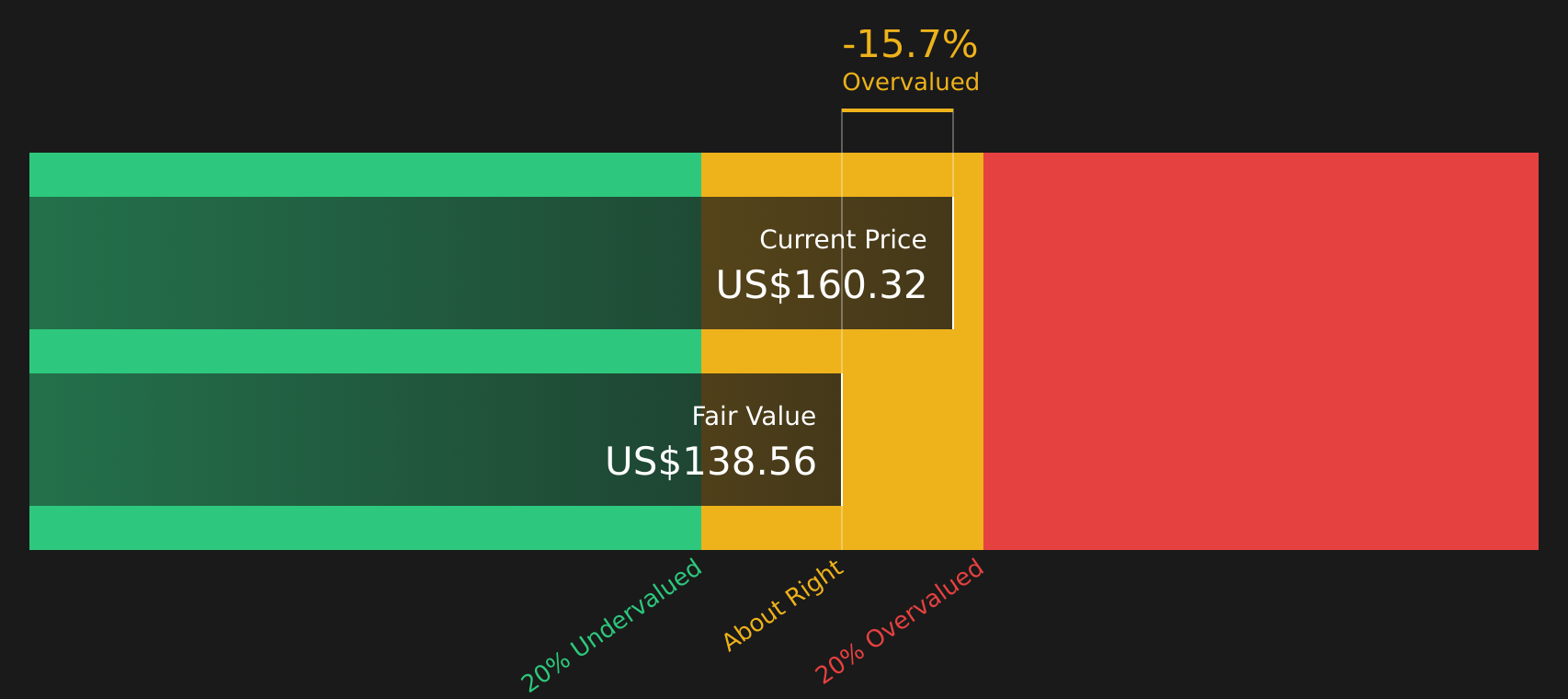

Another View: DCF Paints a Tighter Picture

That 12.2% undervaluation story is only one angle. Our DCF model, which prices Live Nation at $138.56 per share, indicates the stock is trading above its future cash flow value at $160.32, so it is classed as overvalued by this method.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Live Nation Entertainment for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

If the mix of optimism and caution here feels familiar, it is a good moment to look at the numbers yourself and decide quickly where you stand. To see what is driving the positive angles in this story, take a close look at the 1 key reward.

Looking for more investment ideas?

If this story has you thinking more broadly about your portfolio, use the Simply Wall St screener to quickly surface fresh ideas before the crowd does.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’