- In its recently released third-quarter results, Caesars Entertainment reported flat year-over-year revenue at US$2.87 billion and a wider net loss of US$55 million, driven by weaker performance in Las Vegas despite growth in its digital and regional segments.

- This quarter, Caesars also completed a major share buyback and introduced new exclusive slot titles across both digital platforms and physical locations, reflecting ongoing investment in loyalty and product innovation even as traditional Las Vegas operations face headwinds.

- We’ll examine how the softer Las Vegas demand and wider net loss may reshape Caesars Entertainment’s investment narrative going forward.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer’s.

Caesars Entertainment Investment Narrative Recap

To be invested in Caesars Entertainment, you need to believe that growth in digital gaming and improved regional performance can balance or even outweigh persistent challenges in Las Vegas. The latest results show that the recent softness in Las Vegas remains the most important short-term risk, while the continued expansion of Caesars Digital stands out as the biggest catalyst; this quarter’s developments do not materially change that equation.

The launch of exclusive slot titles with AGS is a clear sign of continued investment in Caesars’ digital and cross-channel experiences, reinforcing digital expansion as the core catalyst amid current Las Vegas headwinds. These product launches aim to support customer retention and brand relevance as consumer habits evolve diversifying sources of potential performance improvement even as physical operations face pressure.

But in contrast to the digital upswing, investors need to be aware that if Las Vegas leisure and hospitality demand continues to weaken…

Read the full narrative on Caesars Entertainment (it’s free!)

Caesars Entertainment’s narrative projects $12.6 billion in revenue and $540.9 million in earnings by 2028. This requires a 3.4% yearly revenue growth and a $735.9 million earnings increase from current earnings of -$195.0 million.

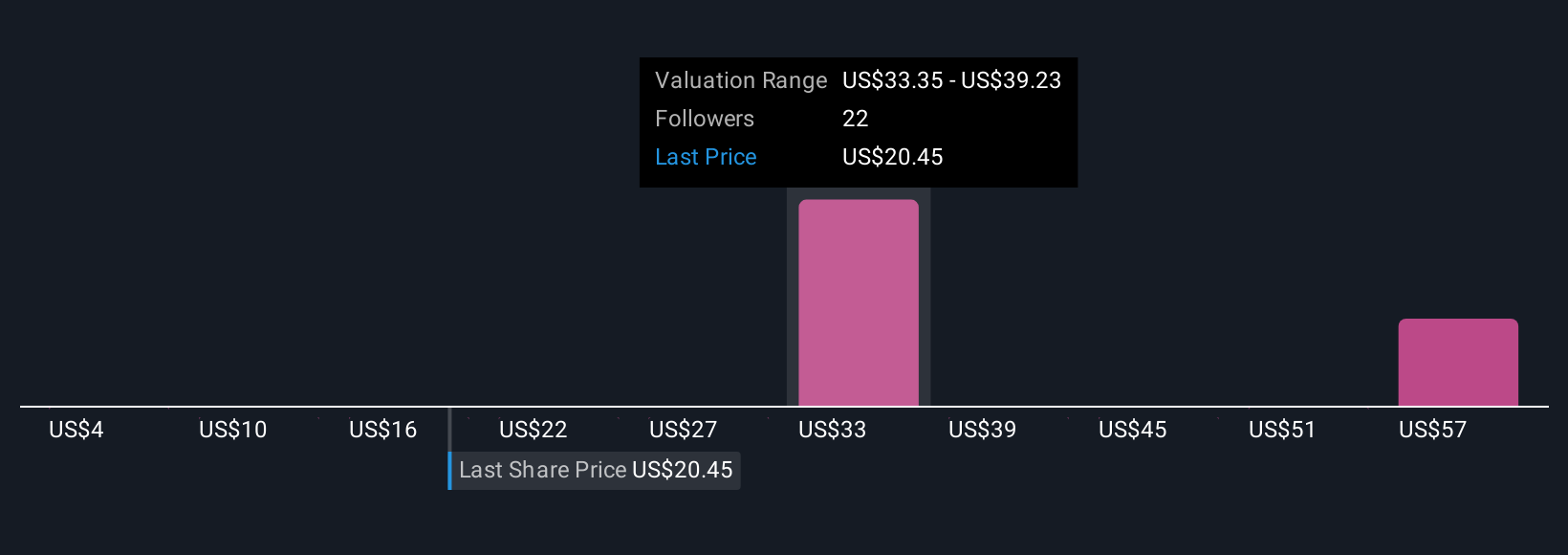

Uncover how Caesars Entertainment’s forecasts yield a $35.88 fair value, a 75% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community recently valued Caesars between US$4 and US$62.71 per share. While opinions differ widely, remember that ongoing Las Vegas weakness could have broader implications for future profitability and capital allocation.

Explore 5 other fair value estimates on Caesars Entertainment – why the stock might be worth over 3x more than the current price!

Build Your Own Caesars Entertainment Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

- A great starting point for your Caesars Entertainment research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Caesars Entertainment research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Caesars Entertainment’s overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don’t delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’