Why Universal Music Group Stock Is On Investors’ Radar

Universal Music Group (ENXTAM:UMG) has caught investor attention after recent share price moves, with the stock showing mixed returns over the past week, month and past 3 months.

That price action is meeting a business that reports €12.5b in revenue and €1.5b in net income, raising questions about how the market is currently valuing one of the largest global music rights owners.

See our latest analysis for Universal Music Group.

Despite the latest 5.4% one day share price decline to €18.79, the recent 7 day share price return of 9.9% contrasts with a weaker 1 year total shareholder return of 17.3%. This suggests momentum has been fading over the longer term as investors reassess growth expectations and risk around UMG’s earnings profile.

If you are weighing up what else could be worth your attention in markets shaped by streaming, copyright and technology, it is a good moment to check out 96 top founder-led companies

With UMG shares trading at €18.79 against a €25.54 analyst price target and recent returns looking mixed, is the current valuation leaving upside on the table, or is the market already pricing in future growth?

Most Popular Narrative: 35% Undervalued

Against the last close at €18.79, the most followed narrative pegs Universal Music Group’s fair value at about €28.90, putting a sizeable gap between price and story.

Increased integration of music across digital lifestyle platforms (health and wellness apps, gaming, streaming video, and short-form social media), as exemplified by UMG’s proprietary AI-driven content partnerships (e.g., Apple Music’s Sound Therapy), opens up new licensing and vertical revenue streams with minimal incremental cost, supporting both revenue diversification and long-term margin expansion.

Curious what kind of revenue mix and margin profile could justify that higher fair value? The narrative leans on recurring digital income, richer tiers, and premium earnings multiples. The numbers behind it are anything but casual.

Result: Fair Value of €28.90 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this hinges on short form platforms becoming better monetised, and on UMG managing potential margin pressure if superstar artists gain more bargaining power.

Find out about the key risks to this Universal Music Group narrative.

Another Way To Look At Valuation

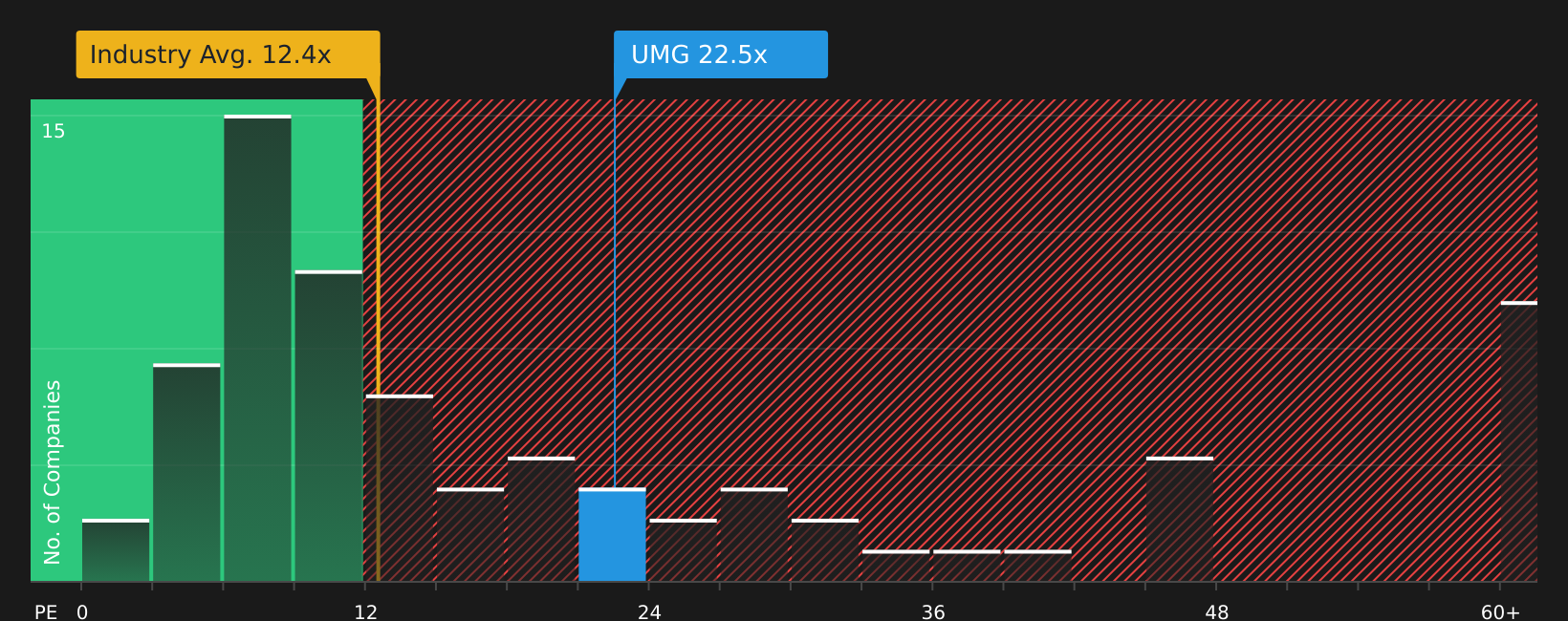

The narrative fair value of €28.90 paints UMG as undervalued, but the current P/E of 22.5x is higher than both the European Entertainment industry at 14.3x and an estimated fair ratio of 14.9x. That richer multiple suggests less margin for error if growth or margins disappoint.

To see what the numbers say about this price, have a look at See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

The mixed tone of this story makes it worth checking the data yourself and forming a clear view sooner rather than later, starting with 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If UMG has sparked your curiosity, do not stop here, use the Simply Wall Street Screener to quickly spot other opportunities that could suit your investing style.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’