Recent share performance and business snapshot

Lucky Strike Entertainment (LUCK) has drawn attention after a recent pullback, with the share price closing at US$7.24 as investors reassess the business following its rebrand from Bowlero Corp.

The company runs a portfolio of bowling centers and entertainment venues across North America, including AMF, Bowl America, Lucky Strike, Bowlero, Octane Raceway, several water parks, and Boomers Parks. It has reported revenue of US$1,240.203 million and a net income loss of US$94.314 million.

See our latest analysis for Lucky Strike Entertainment.

The recent 1 day share price return of a 3.85% decline and 7 day share price return of a 19.56% decline cap a year where total shareholder return is down 21.13%, with the longer term 3 year total shareholder return of a 47.96% decline pointing to fading momentum as investors reassess the rebranded business and its loss making profile.

If this kind of reset has you reassessing your watchlist, it can help to broaden the search with companies tied to long term secular themes such as 33 power grid technology and infrastructure stocks

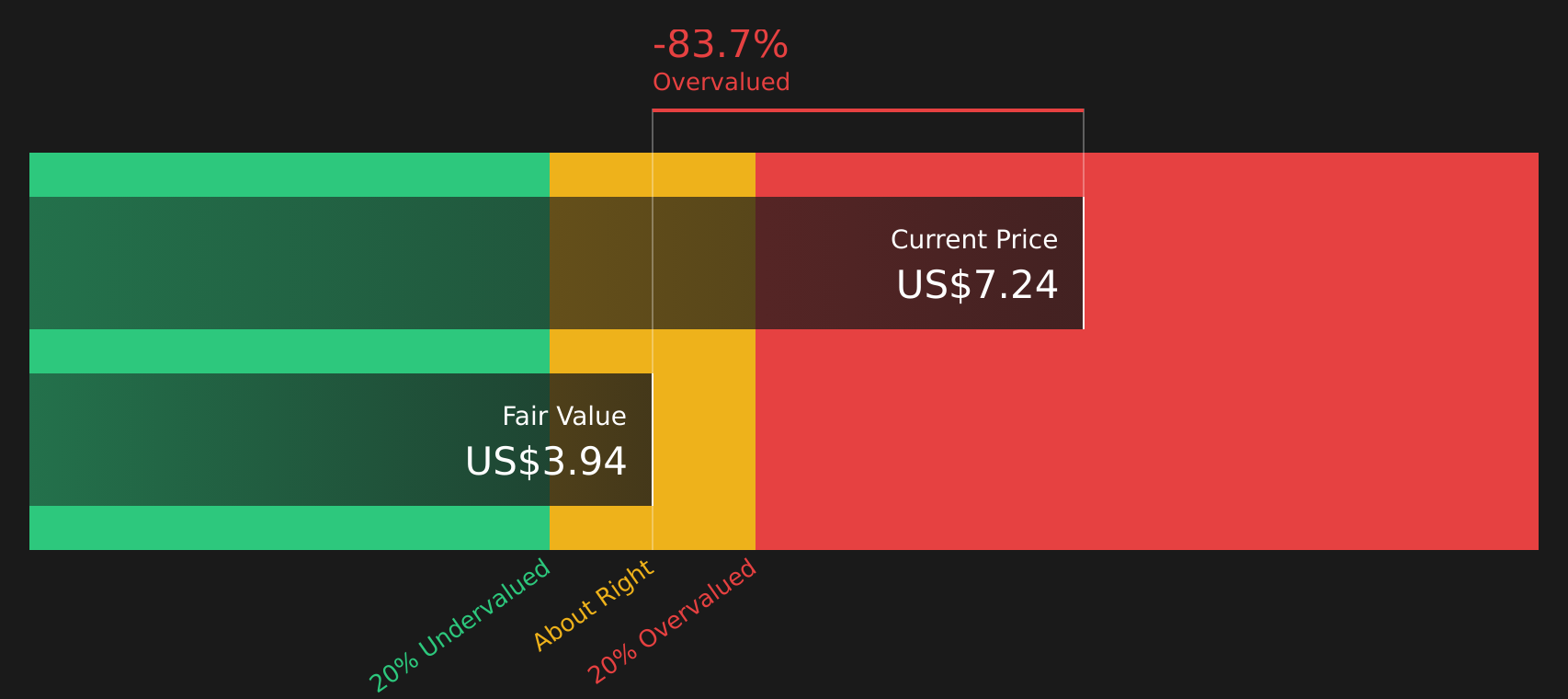

With Lucky Strike Entertainment trading at US$7.24 against an analyst price target of US$10.89, along with a loss of US$94.314 million on US$1,240.203 million of revenue, should you see value here or assume markets are already pricing in future growth?

Most Popular Narrative: 33.5% Undervalued

With Lucky Strike Entertainment last closing at $7.24 against a narrative fair value of $10.89, the widely followed story centers on venue expansion, brand refresh, and efforts to improve margins from a loss making base.

The conversion of Bowlero locations to Lucky Strike, alongside targeted, higher-return marketing spend and refreshed branding, is already showing early signs of comp improvement in key markets and is expected to meaningfully accelerate same-store sales and operating leverage as the transition scales system-wide.

Want to see what sits behind that confidence in higher comps and operating leverage? The narrative leans heavily on revenue growth, margin expansion, and a richer earnings profile built around these assumptions.

Result: Fair Value of $10.89 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, you also need to weigh risks, such as high fixed costs tied to US$1.3b of net debt and rising competition from alternative entertainment options that may pressure visits and margins.

Find out about the key risks to this Lucky Strike Entertainment narrative.

Another way to look at value

The narrative fair value of $10.89 suggests upside, but the SWS DCF model points in the opposite direction, with an estimate of $3.95 and a view that LUCK at $7.24 is trading above its future cash flow value. Which story about future cash generation do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If this mix of risks and potential rewards leaves you unsure, it is worth reviewing the numbers yourself and deciding where you stand. To help frame both sides of the story in one view, take a look at the 1 key reward and 2 important warning signs

Looking for more investment ideas?

If this story has sparked fresh thinking about your portfolio, do not stop here. Broaden your opportunity set and let the data work harder for you with a few focused stock lists.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’