China Star Entertainment (SEHK:326) just released full year 2025 results showing revenue of HK$404.92 million and a net loss of HK$443.76 million, broadly in line with guidance for a sizeable annual loss.

See our latest analysis for China Star Entertainment.

The weak 2025 results come after a sharp re-rating in the market, with the share price at HK$6.70 and a 30 day share price return of 45.34%. This has fed into a very large 1 year total shareholder return, suggesting momentum has been building even as reported losses remain substantial.

If you are looking beyond China Star Entertainment for other opportunities in this part of the market, it could be a good time to scan 94 top founder-led companies

With the share price soaring and losses still heavy, this suddenly looks very different from the low profile media stock it once was. So is China Star Entertainment now undervalued, or has the market already priced in future growth?

Preferred Price-to-Sales Multiple of 40.2x: Is it justified?

China Star Entertainment is currently valued at a P/S of 40.2x, which is very high compared to both its peer group average of 3.3x and the Hong Kong Entertainment industry average of 1.7x. That lofty multiple sits on top of a business that is still loss making, with a net loss of HK$443.76 million against revenue of HK$404.92 million.

The P/S ratio compares the company’s market value with its revenue, so a higher multiple usually reflects strong expectations for future sales or a premium attached to the business model. In this case, the market is assigning a price tag that is many times higher than what is typical among similar entertainment names, even though there is no clear profitability signal in the recent numbers.

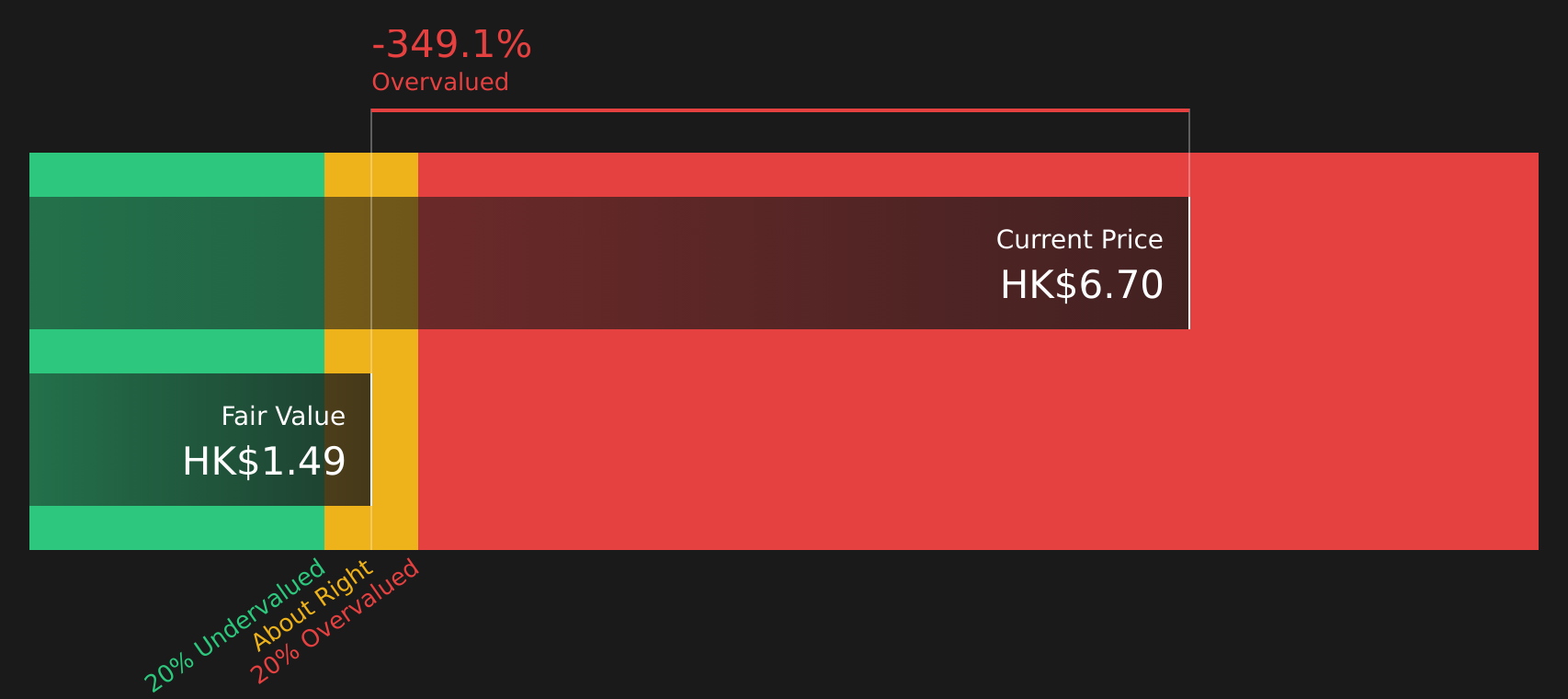

Compared to peers on 3.3x sales and the wider Hong Kong Entertainment industry on 1.7x, China Star Entertainment’s 40.2x P/S stands out as expensive in relative terms. The SWS DCF model also estimates a future cash flow value of HK$1.49 per share, while the stock trades at HK$6.70, which points to a large premium over that implied fair value.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-sales of 40.2x (OVERVALUED)

However, heavy HK$443.76 million losses and a very high 40.2x P/S multiple mean that any disappointment in revenue or capital raising could quickly pressure the story.

Find out about the key risks to this China Star Entertainment narrative.

Another View: Cash Flows Point To A Different Story

The SWS DCF model values China Star Entertainment at HK$1.49 per share, well below the current HK$6.70 price. This suggests the shares look expensive using cash flow assumptions as well as sales multiples. If both signals indicate a rich valuation, what exactly is the market paying up for?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out China Star Entertainment for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 240 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

If this all sounds cautious, that is the point. It is worth checking the data for yourself before the next move starts to form in the market. To round out your view and see what concerns others are flagging, take a closer look at the 2 important warning signs

Looking for more investment ideas?

If China Star Entertainment feels too finely balanced, do not stop there. Broaden your watchlist now so you are not chasing stories after they move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’