What Live Nation Entertainment’s Recent Performance Tells Current Shareholders

Live Nation Entertainment (LYV) has been on many investors’ watchlists after a mixed stretch in the stock, with short term returns under pressure while longer term performance remains positive.

Over the past day, week, month, and past 3 months, the shares have shown returns of roughly 1.0%, 2.6%, 0.9%, and 4.5% declines respectively, compared with modestly negative performance year to date and over the past year.

In contrast, Live Nation’s 3 year and 5 year total returns, at roughly 80% and 88%, indicate that longer holding periods have looked different from the more recent pullback.

The company reports annual revenue of about US$24.6b and net income of roughly US$322.2m. The supplied revenue and net income growth rates are 7.7% and 41.0% respectively, which helps frame how the current share price of US$143.94 sits against its recent fundamentals.

See our latest analysis for Live Nation Entertainment.

For current shareholders, the recent share price pressure, including a 4.5% 3 month share price return decline and slightly negative 1 year total shareholder return, contrasts with the much stronger 3 and 5 year total shareholder returns. This suggests that momentum has been fading in the short term while longer term holders have still seen meaningful gains.

If Live Nation’s recent pullback has you reassessing your options, it could be a good moment to broaden your watchlist with fast growing stocks with high insider ownership.

So with the share price easing off recent highs, while 3 and 5 year returns remain in positive territory and revenue is about US$24.6b, is Live Nation now trading below its worth, or is the market already pricing in future growth?

Most Popular Narrative: 15.1% Undervalued

Against Live Nation Entertainment’s last close of $143.94, the most followed narrative pegs fair value at about $169.48, implying upside that the current share price does not yet reflect, based on its cash flow and earnings profile.

The experience economy is fueling robust, sustained consumer demand for concerts and festivals worldwide, as evidenced by record ticket sales, growing international fan attendance, and strong sell through rates; this dynamic underpins continued top line expansion and higher on site spending per event, supporting both revenue and margin growth.

Curious what kind of revenue pace, margin lift, and future earnings power are baked into that fair value math? The core assumptions may surprise you. The pricing multiple that ties it all together is even more so.

Result: Fair Value of $169.48 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this hinges on key risks, including prolonged regulatory scrutiny around Ticketmaster and a softer North American outlook that could pressure margins and challenge those fair value assumptions.

Find out about the key risks to this Live Nation Entertainment narrative.

Another Angle On Valuation

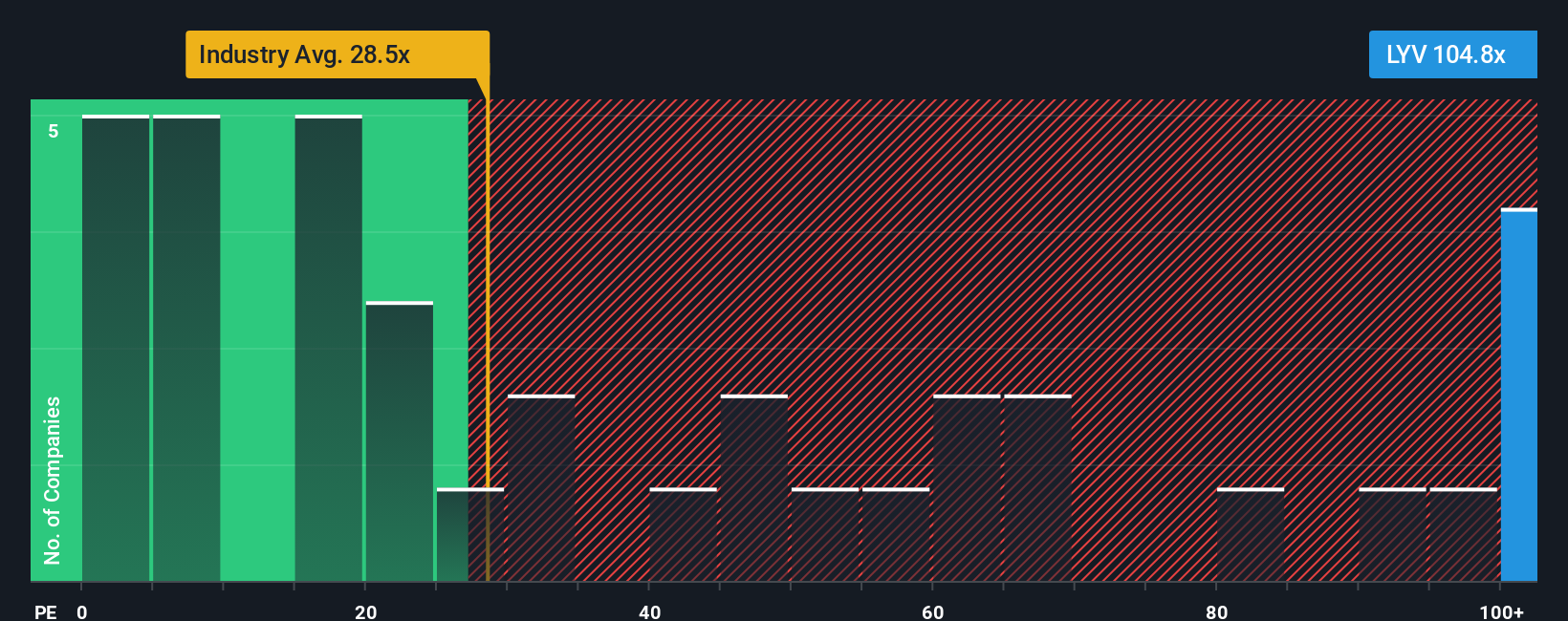

So far you have seen a narrative that points to Live Nation looking undervalued, but the P/E picture tells a different story. On current numbers, the shares trade on a P/E of 103.7x, compared with 56.4x for peers and 30.1x for the broader US Entertainment industry.

The fair ratio is 40.8x, which is less than half of where the shares sit today. That gap suggests valuation risk if sentiment cools, rather than a clear pricing cushion. The key question for you is whether Live Nation’s future earnings can grow enough to close that gap instead of the multiple doing it.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Live Nation Entertainment Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom thesis in just a few minutes: Do it your way.

A great starting point for your Live Nation Entertainment research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready For More Investment Ideas?

If Live Nation has sharpened your thinking, do not stop here. The real edge often comes from comparing a few clear ideas side by side.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’