Flutter Entertainment (FLUT) is back in focus after its latest earnings update, which paired a 16.8% year-on-year revenue increase and an EBITDA beat with missed revenue and EPS expectations and an 8.6% stock decline.

See our latest analysis for Flutter Entertainment.

At a share price of $201.08, Flutter’s recent 8.6% post earnings drop sits within a wider losing patch, with a 30 day share price return of 8.33% and a 1 year total shareholder return decline of 21.93%. However, the 3 year total shareholder return of 32.77% points to earlier momentum that has faded more recently.

If you are comparing Flutter’s recent swings with other opportunities in online betting and gaming, it could be worth widening your search to fast growing stocks with high insider ownership to see what else stands out.

With Flutter trading at $201.08 and sitting below some implied value estimates, the key question is whether recent earnings disappointment has created a genuine mispricing or if the current level already reflects its future growth potential.

Most Popular Narrative: 32% Undervalued

Against Flutter Entertainment’s last close of $201.08, the most followed narrative points to a fair value of about $295.63 based on a detailed long term cash flow outlook discounted at 9.27%.

Structural cost efficiencies, evidenced by reduced sales and marketing as a percentage of revenue and successful renegotiation of market access agreements (e.g., Boyd), should drive higher net margins and enhanced free cash flow, supporting shareholder returns through buybacks.

Curious what has to happen to margins, revenue and earnings for that valuation to stack up, and how long growth needs to hold up to support it? The narrative lays out those assumptions step by step.

Result: Fair Value of $295.63 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are also clear warning signs, including rising regulatory and tax pressure in key markets, as well as high net debt of about US$8.5b that could squeeze returns.

Find out about the key risks to this Flutter Entertainment narrative.

Another Angle on Valuation

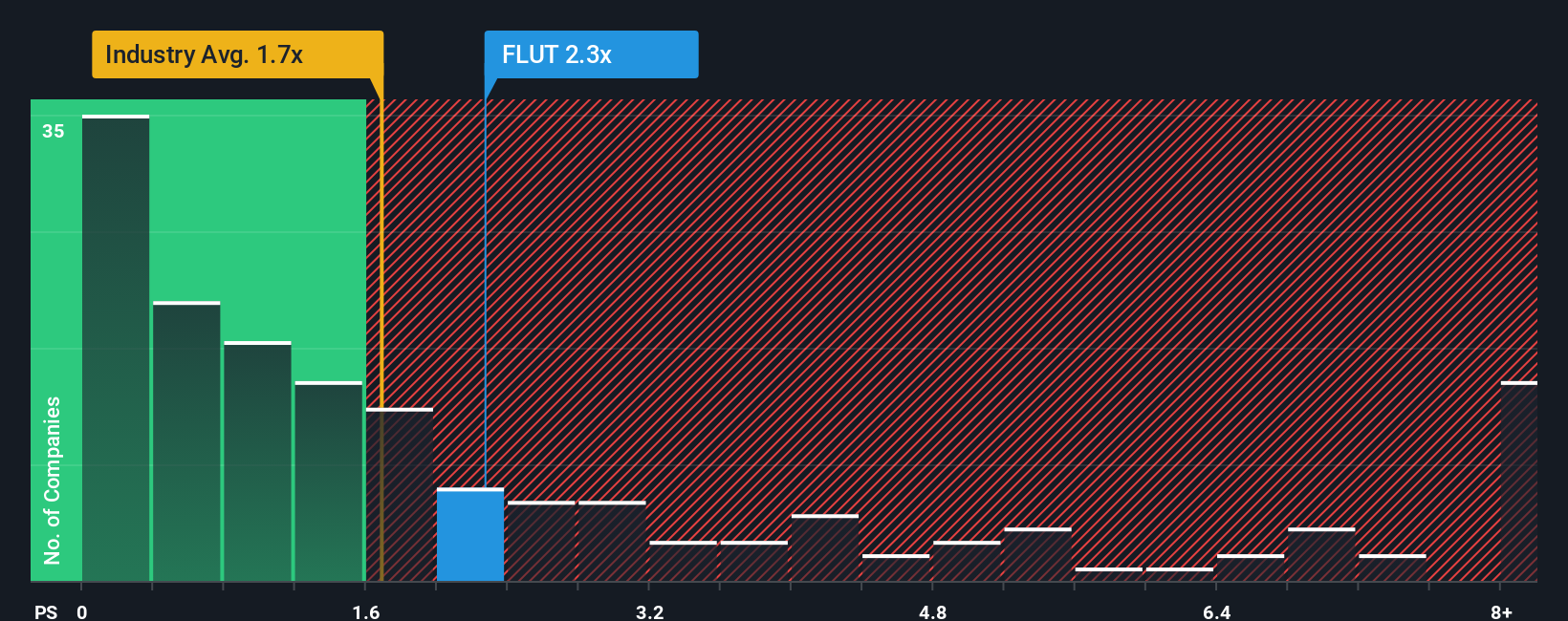

On one hand, Flutter screens as good value compared with its own fair ratio, with a P/S of 2.3x versus a fair ratio estimate of 3.8x. On the other, it looks expensive against the US Hospitality industry at 1.7x and a peer average of 2.2x. Which reference point do you trust more?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Flutter Entertainment Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a personalised Flutter view in minutes. To get started, use Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Flutter Entertainment.

Ready to hunt for more ideas?

If Flutter has you thinking about what else might be interesting right now, do not stop here. Use the Simply Wall St Screener to quickly surface fresh opportunities that fit your style.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’