If you are wondering whether Flutter Entertainment’s current share price lines up with its underlying worth, you are not alone. This article focuses on what the numbers say about value.

The stock trades at US$199.85, with returns of a 5.5% decline over 7 days, a 9.0% decline over 30 days, an 8.4% decline year to date, a 21.7% decline over 1 year and a 30.7% gain over 3 years, alongside a 0.2% gain over 5 years. This raises questions about how the market is reassessing risk and opportunity over different time frames.

Recent news coverage around Flutter Entertainment has largely centered on its position in global online betting and gaming markets and ongoing attention from investors to regulatory developments in key regions. Together, these themes help frame why sentiment and pricing can shift quickly as the market reassesses future cash flow expectations and perceived risks.

Our valuation work gives Flutter Entertainment a 4 out of 6 valuation score, suggesting several checks point to potential undervaluation, while others are more balanced. Next we will walk through standard valuation approaches and, by the end, return to an even more helpful way to think about what the current share price really implies.

A Discounted Cash Flow model projects the cash a business could generate in the future and then discounts those cash flows back to today, to estimate what the entire company might be worth in current dollars.

ADVERTISEMENT

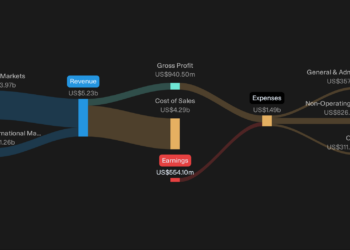

For Flutter Entertainment, the model uses a 2 Stage Free Cash Flow to Equity approach, starting from last twelve months free cash flow of about $687.8 million. Analyst-based and extrapolated estimates then project free cash flow each year out to 2035, with forecast free cash flow in 2030 of about $4.5b and a terminal stage that grows more slowly after that. These projections are all in $, even though the shares themselves trade in US$.

Adding up the discounted values of those future cash flows gives an estimated intrinsic value of about $383.99 per share. Against the current share price of US$199.85, the model implies the shares trade at a 48.0% discount to this estimate, which indicates the stock may be undervalued on this set of cash flow assumptions.

For companies where investors focus on revenue scale and market share, the P/S ratio is often a useful cross check because it compares the value of the equity to the sales the business is already generating.

In general, stronger growth expectations and lower perceived risk can support a higher P/S multiple, while slower growth and higher risk tend to align with a lower, more conservative range.

Flutter Entertainment currently trades on a P/S of about 2.27x. That sits slightly above the Hospitality industry average of 1.68x and above the peer group average of 2.17x, which suggests the market is placing a somewhat richer value on each dollar of Flutter Entertainment sales than on its industry or peer group overall.

Simply Wall St also calculates a proprietary “Fair Ratio” of 3.85x for Flutter Entertainment. This is the P/S level that might be expected given factors such as earnings growth, profit margins, industry, market cap and company specific risks.

This Fair Ratio can be more informative than a simple industry or peer comparison because it adjusts for the quality and risk profile of the business rather than assuming all companies deserve the same multiple.

Comparing the Fair Ratio of 3.85x with the current P/S of 2.27x indicates that the shares trade below this model based estimate of a fair P/S level.

Earlier we mentioned that there is an even better way to think about valuation. On Simply Wall St that starts with Narratives, where you set out your story for Flutter Entertainment, link it to a concrete forecast for revenue, earnings and margins, and let the platform turn that into a fair value you can compare with the current price on the Community page that millions of investors use.

A Narrative is simply your view of what is driving Flutter Entertainment, written in plain language, then backed up by numbers such as what you think future earnings might look like, what P/E you are comfortable using and what discount rate fits the risk you see.

This turns your story into a full valuation that updates automatically when new earnings, guidance or news arrive. You can quickly see whether your fair value now sits above or below the live share price and then decide if the gap is wide enough for you to consider buying, holding or selling.

For example, one Flutter Entertainment Narrative on Simply Wall St currently values the shares at about US$393 per share, while another is closer to US$267 per share. This shows how two investors using the same public information can reach different fair values based on their own expectations for U.S. liberalization, U.K. gaming taxes, margins and growth. You can place yourself on that spectrum with your own Narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.