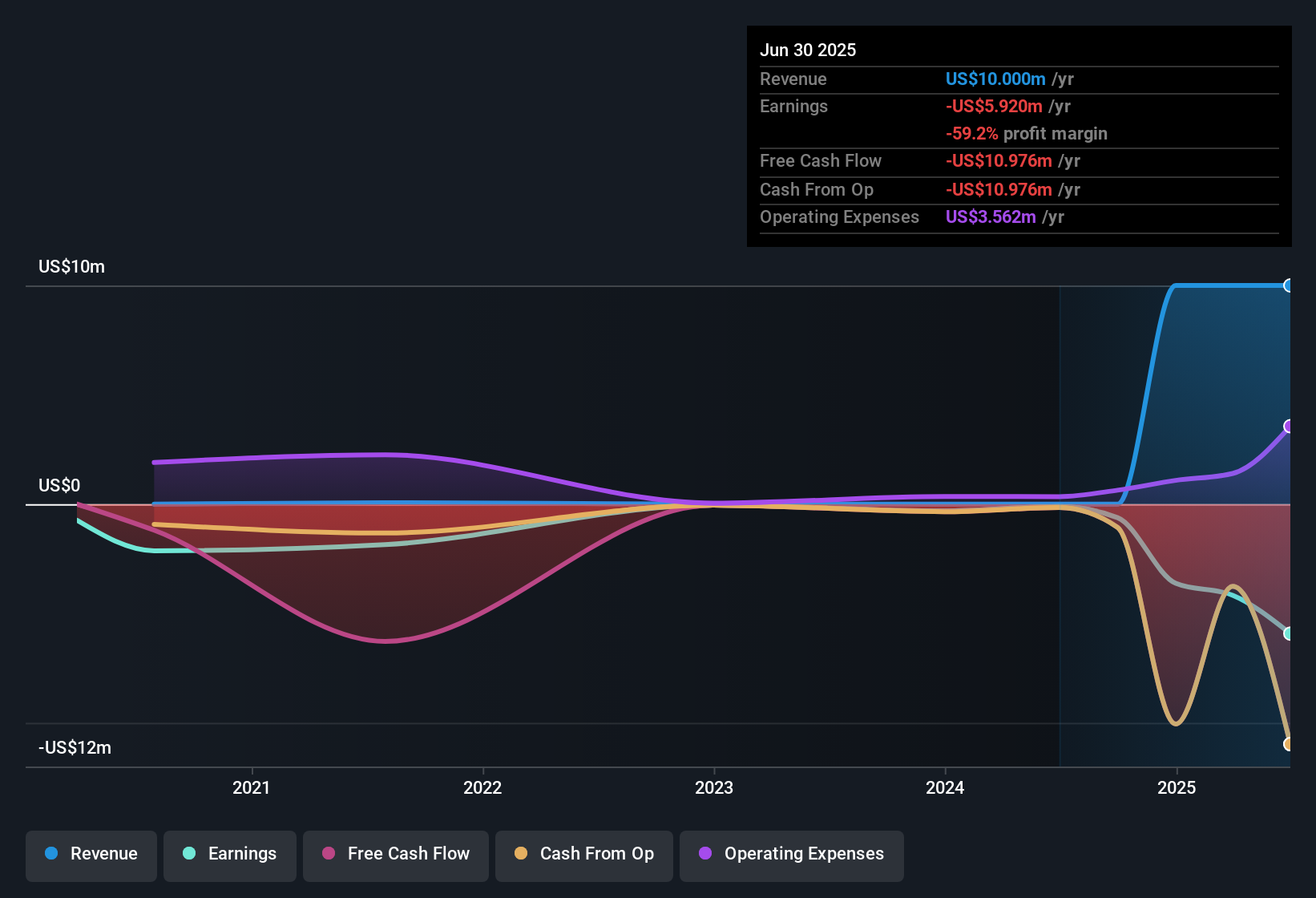

Rivulet Entertainment (RIVF) remains unprofitable, with net losses increasing at an average rate of 20.7% per year over the past five years. The company’s Price-To-Sales Ratio sits at 13.7x, which is a substantial premium over the US software industry average of 5.1x and its peer group average of 3.4x. As ongoing losses show no sign of abating and key profitability metrics have yet to improve, investors may view the latest results with understandable caution.

See our full analysis for Rivulet Entertainment.

Next, we will look at how these earnings figures compare with the broader market narrative and what they mean for the stock’s outlook.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Accelerate Despite High Sales Multiple

- Net losses have been growing at an average rate of 20.7% per year for the past five years, with no reversal in sight according to the latest filings.

- While prevailing market analysis notes that entertainment sector companies sometimes justify premium multiples with strong content pipelines or successful adaptation to digital trends, Rivulet’s continued losses and absence of high-quality past earnings offer little evidence in support of such a bull case.

- The filings confirm there has not been any improvement in net profit margin or quality of earnings. This undercuts optimism around the company’s ability to grow into its valuation.

- Questions remain about the company’s capacity to deliver major entertainment projects that could alter this loss trajectory, given the lack of revenue or earnings growth forecasts.

Financial Position Fails to Support Turnaround

- No evidence of positive equity or a strengthening financial position has been disclosed, and all major risks flagged remain unresolved in the current financials.

- Critics highlight that, unlike some peers who show clear paths to profitability with effective cost controls, Rivulet faces ongoing risks associated with weak fundamentals.

- The company’s lack of revenue and earnings growth potential stands out, as risks to both cash flow and valuation remain at the forefront in the latest disclosure.

- Additionally, share price instability over the past three months signals that investors do not yet see a compelling fundamental turnaround case.

Valuation Stays Stretched Versus Peers

- With a Price-To-Sales Ratio of 13.7x, which is well above the US software industry average of 5.1x and peer group average of 3.4x, the company remains priced at a steep premium despite its ongoing losses and lack of profitability improvements.

- Prevailing market analysis points out that such an elevated valuation typically requires either high growth or significant market share wins, neither of which are evidenced here.

- The absence of positive earnings or clear revenue catalysts challenges the justification for RIVF’s valuation premium in the current market context.

- This further amplifies cautious sentiment toward the stock, especially as all major identified risks remain firmly in place.

Next Steps

Don’t just look at this quarter; the real story is in the long-term trend. We’ve done an in-depth analysis on Rivulet Entertainment’s growth and its valuation to see if today’s price is a bargain. Add the company to your watchlist or portfolio now so you don’t miss the next big move.

See What Else Is Out There

Rivulet Entertainment’s mounting losses, lack of profitability progress, and a stretched valuation highlight significant concerns about its financial health and turnaround potential.

If you want stronger fundamentals and lower risk, check out solid balance sheet and fundamentals stocks screener (1987 results) to find companies with proven balance sheets and financial resilience built in.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’