Sphere Entertainment (SPHR) is back in focus after highlighting strong momentum in its immersive shows, including The Wizard of Oz at Sphere, and announcing a new Rocky Horror Picture Show experience, along with plans for additional global venues.

See our latest analysis for Sphere Entertainment.

That momentum is clearly reflected in Sphere Entertainment’s recent trading, with a 1-month share price return of 16.26% and a year to date share price return of 66.84%. The 1-year total shareholder return exceeds 3x and points to strong positive sentiment building around its immersive venue rollout and content slate.

If Sphere Entertainment’s run has you thinking about what else is moving, this could be a good moment to widen your search and uncover 20 top founder-led companies

With Sphere Entertainment now trading near US$157 and sitting only about 12% below an estimated intrinsic value and 8% under the average analyst target, the key question is whether there is still a mispricing here or if the market is already factoring in future growth.

Most Popular Narrative: 2% Undervalued

Sphere Entertainment is trading at $157.33, a touch below a narrative fair value of $161.00. This frames the recent share price strength against long term earnings expectations built into that model.

The expansion into new markets, particularly the development of both full-size and smaller franchise-model Spheres internationally (such as in Abu Dhabi and potential other cities), directly positions Sphere Entertainment to benefit from the increasing demand for experiential destination entertainment, supporting long term revenue growth and margin scalability through asset-light models. Increasing consumer appetite for immersive, tech-driven live experiences, supported by rapid advancements in AI and next-gen display technologies, underpins Sphere’s unique content offerings (e.g., Wizard of Oz at Sphere). This enables the company to achieve premium ticket pricing and improved per-event margins as expectations for high-quality, multi-sensory events rise.

Want to see what sits behind that fair value gap for Sphere Entertainment? The narrative leans on measured revenue growth, firmer margins and a richer future earnings multiple. Curious which specific forecast shifts and discount rate assumptions are doing the heavy lifting here? The full breakdown joins those threads together for you.

Result: Fair Value of $161.00 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the Sphere Entertainment story also hinges on tourism holding up and on new venues, such as Abu Dhabi or Nashville, avoiding cost overruns or softer demand.

Find out about the key risks to this Sphere Entertainment narrative.

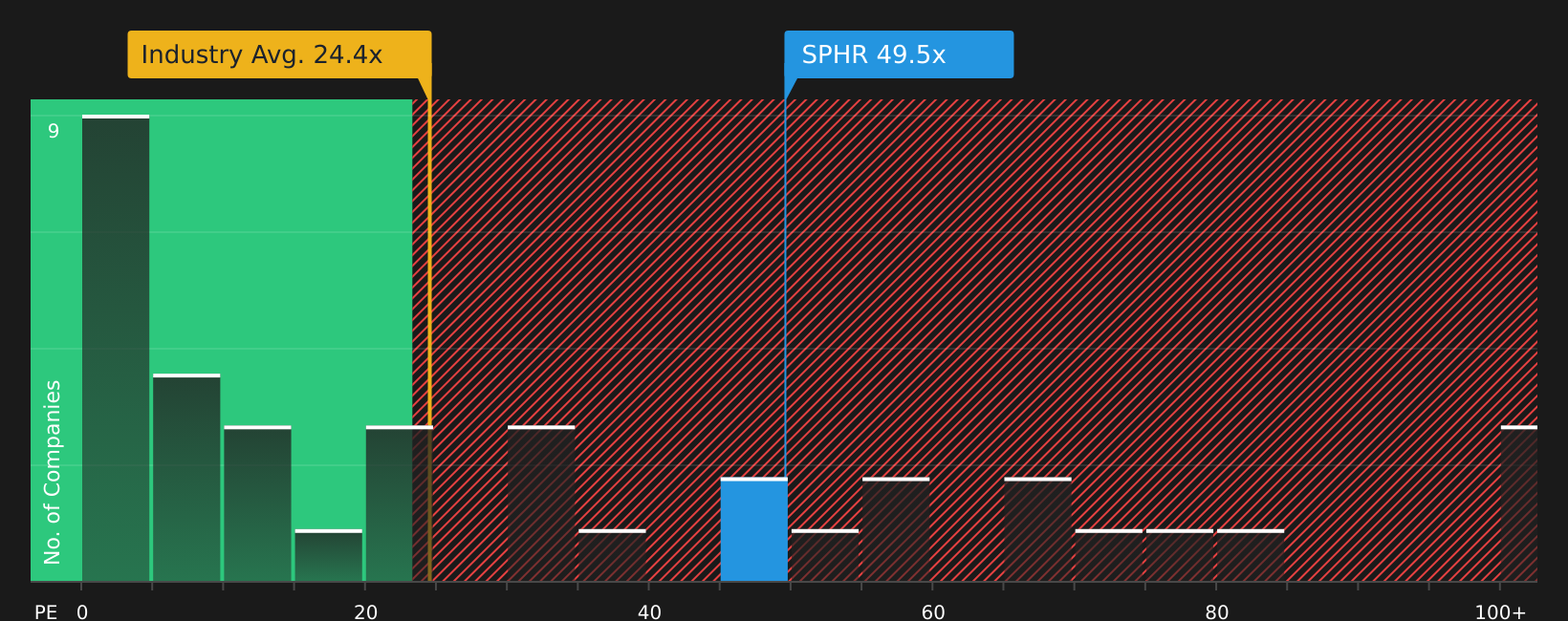

Another View: Sphere Entertainment Through Earnings Multiples

The earlier narrative paints Sphere Entertainment as slightly undervalued against a $161.00 fair value, yet the picture looks different when price is compared with earnings. SPHR trades on a P/E of 49.5x, which is more expensive than the US Entertainment industry at 24.2x, the peer group at 42.7x, and a fair ratio of 3.4x that the market could move towards over time. That gap raises a practical question for investors, whether recent excitement around Sphere’s venues justifies paying this kind of premium for every dollar of earnings.

To see how the current earnings multiple stacks up in more detail, and what that might mean for valuation risk, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Does the mix of enthusiasm and caution around Sphere Entertainment feel justified to you, or not quite? Take a closer look at the details, weigh the potential upside against the concerns, and see the full picture by checking out the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Sphere Entertainment?

If Sphere Entertainment has sharpened your focus on where capital goes next, do not stop here. Use this moment to line up your next few watchlist candidates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’