- In the first quarter of 2026, Caesars Entertainment reported higher sales of US$2,153 million and revenue of US$2,870 million, while reducing its net loss to US$98 million compared with the prior year.

- Alongside these improved results, Caesars has been expanding its entertainment offerings with new venues such as OMNIA Dayclub & Skybar in Las Vegas and the upcoming Caesars Beach Club in Atlantic City, aiming to draw more visitors to its properties.

- Next, we will examine how Caesars’ narrowed quarterly loss and new property openings may influence its broader investment narrative.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Caesars Entertainment Investment Narrative Recap

To own Caesars Entertainment, you need to believe the company can turn modest revenue growth and its large casino footprint into consistent profitability while managing its significant debt load. The latest quarter showed slightly higher revenue and a narrower net loss, which modestly supports that thesis, but continued losses and leverage still look like the key near term risk, especially if softer demand or higher costs persist.

The opening of OMNIA Dayclub & Skybar at Caesars Palace fits into this story as a fresh attempt to keep Las Vegas properties relevant and appealing. New venues like OMNIA and the upcoming Caesars Beach Club in Atlantic City are designed to increase traffic and non gaming spend, which could help offset pressure from promotions and reinvestment costs if they translate into stronger property level performance.

Yet while these openings are exciting, investors should also weigh the ongoing risk that heavy marketing spend and high leverage could still pressure Caesars’ cash flow and…

Read the full narrative on Caesars Entertainment (it’s free!)

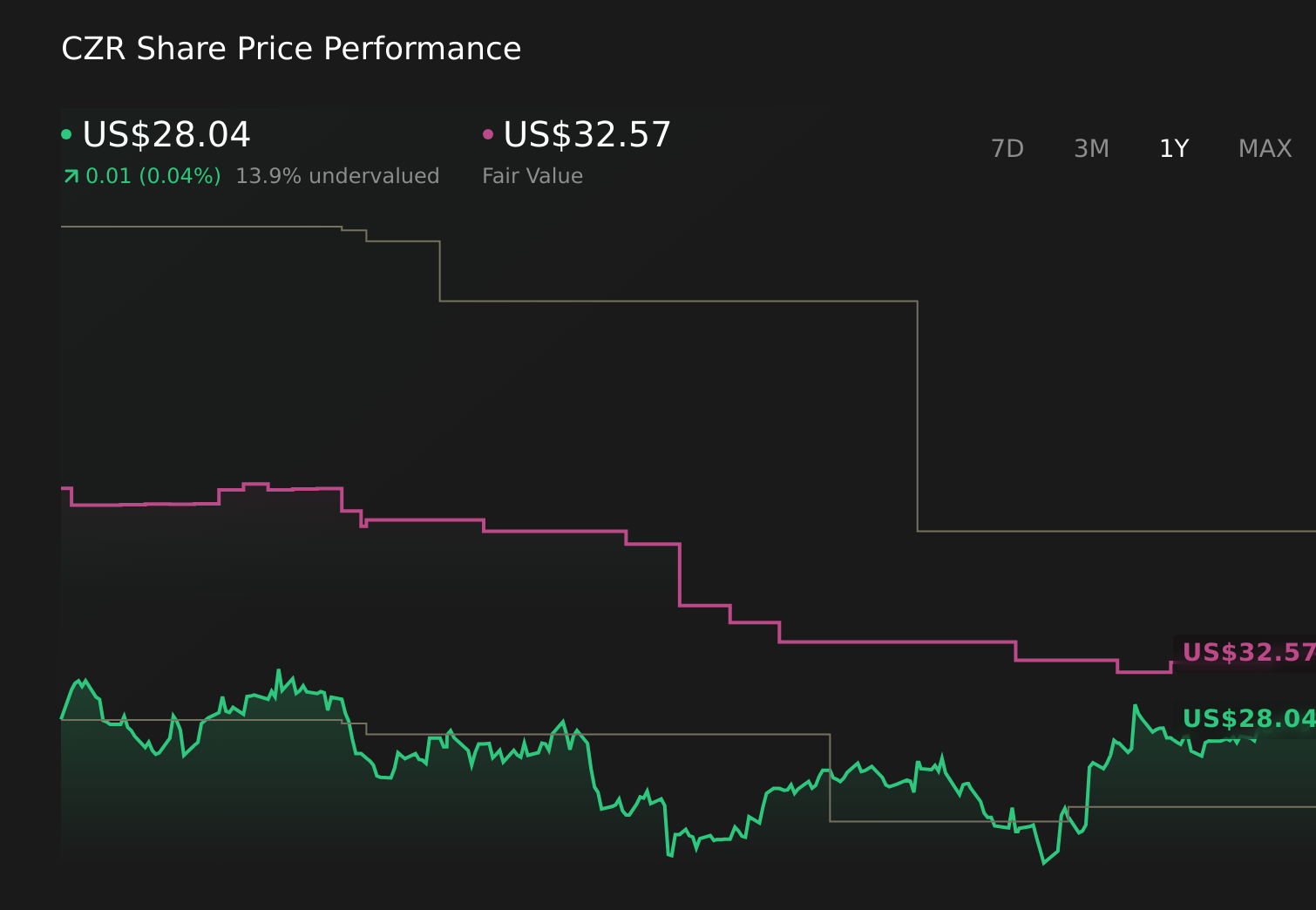

Caesars Entertainment’s narrative projects $12.3 billion revenue and $230.7 million earnings by 2029.

Uncover how Caesars Entertainment’s forecasts yield a $32.57 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much tougher picture, assuming only about 1.8% annual revenue growth and earnings of roughly US$47 million by 2029, which contrasts sharply with the more optimistic view that recent earnings progress and new properties will steadily improve margins.

Explore 3 other fair value estimates on Caesars Entertainment – why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Caesars Entertainment research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Caesars Entertainment research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Caesars Entertainment’s overall financial health at a glance.

Contemplating Other Strategies?

The market won’t wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’