- Sphere Entertainment Co. reported past first-quarter 2026 results with sales of US$386.41 million versus US$280.57 million a year earlier, while net loss narrowed to US$1.59 million from US$81.95 million and loss per share from continuing operations improved to US$0.04 from US$2.27.

- Despite this operational improvement, the company now faces a tougher backdrop as record-low consumer sentiment and rising household cost pressures weigh on demand for discretionary leisure experiences.

- With earnings improving but consumer sentiment weakening, we’ll explore how these macro headwinds could influence Sphere Entertainment’s investment narrative.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Sphere Entertainment Investment Narrative Recap

To own Sphere Entertainment, you have to believe its immersive venues can keep drawing paying audiences and sponsors even as consumer budgets tighten. The latest quarter showed higher sales and a sharply reduced net loss, which supports the near term catalyst of better profitability, but the record low consumer sentiment highlights the key risk that demand for premium live experiences could soften. For now, the earnings beat does not fully offset concerns about weaker discretionary spending.

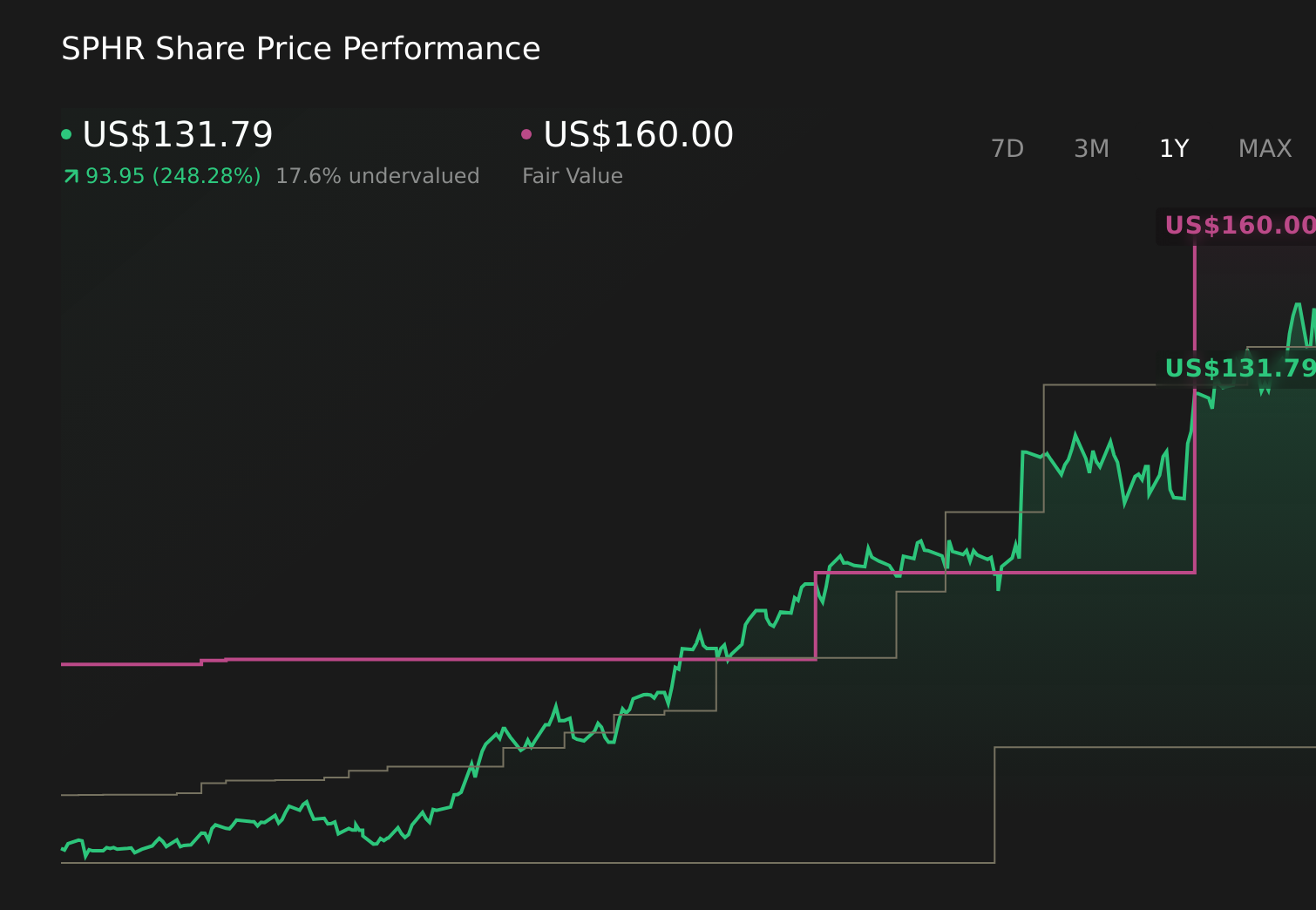

The first quarter 2026 earnings release is the most relevant recent announcement here. It shows sales rising to US$386.41 million and net loss narrowing to US$1.59 million, suggesting the core venue and content model can generate improving results even before any major expansion. How durable that improvement proves, especially with Sphere investing heavily in new content like The Wizard of Oz and other Sphere Experiences, will be central to how investors think about future catalysts and risk.

Yet behind Sphere’s improving numbers, there is a risk investors should be aware of if consumer budgets stay under pressure and…

Read the full narrative on Sphere Entertainment (it’s free!)

Sphere Entertainment’s narrative projects $1.3 billion revenue and $128.8 million earnings by 2029. This requires 2.5% yearly revenue growth and a $95.4 million earnings increase from $33.4 million today.

Uncover how Sphere Entertainment’s forecasts yield a $136.36 fair value, a 3% upside to its current price.

Exploring Other Perspectives

While consensus sees Sphere growing, the most pessimistic analysts were assuming only about 6 percent annual revenue growth and no profitability by 2028, which highlights how differently you might weigh today’s consumer stress against Sphere’s high fixed costs and premium pricing power.

Explore 3 other fair value estimates on Sphere Entertainment – why the stock might be worth as much as 58% more than the current price!

Form Your Own Verdict

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’