Accel Entertainment trades at $12.76 per share and has stayed right on track with the overall market, gaining 12.2% over the last six months. At the same time, the S&P 500 has returned 9.3%.

Why Do We Think Accel Entertainment Will Underperform?

We don’t have much confidence in Accel Entertainment. Here are three reasons we avoid ACEL, plus one stock we’d rather own.

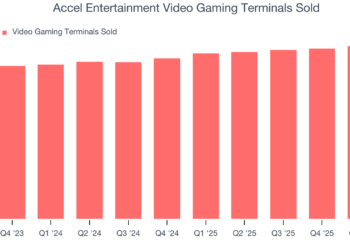

1. Weak Growth in Video Gaming Terminals Sold Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Accel Entertainment, our preferred volume metric is video gaming terminals sold). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Accel Entertainment’s video gaming terminals sold came in at 28,353 in the latest quarter, and over the last two years, averaged 6.1% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Accel Entertainment has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.9%, below what we’d expect for a consumer discretionary business.

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Over the last few years, Accel Entertainment’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Accel Entertainment doesn’t pass our quality test. That said, the stock currently trades at 13.3× forward P/E (or $12.76 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source www.tradingview.com ’