Global In-Flight Entertainment Summary

Market Size & Growth

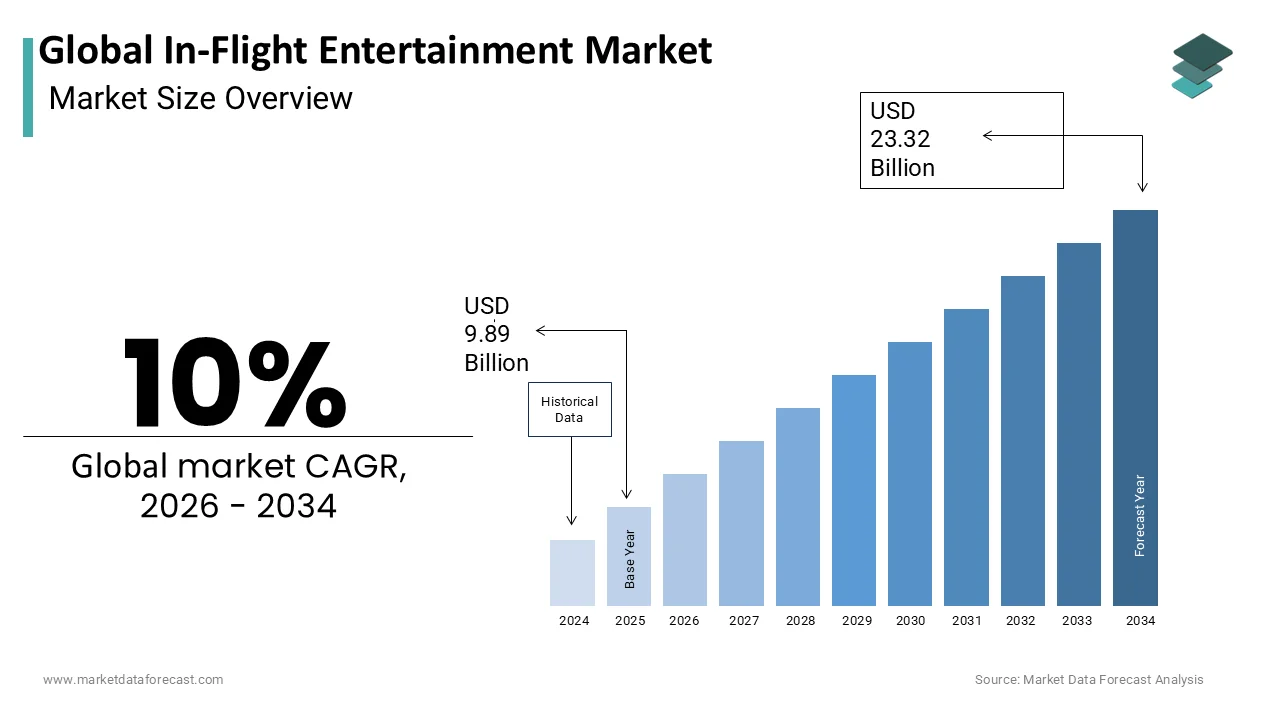

- The Global In-Flight Entertainment market was valued at USD 9.89 billion in 2025.

- Expected to reach USD 10.88 billion in 2026 and USD 23.32 billion by 2034, growing at a CAGR of 10% from 2026 to 2034.

- The IFE Connectivity segment is the fastest-growing, at a CAGR of 18.2% from 2026 to 2034.

Key Market Segments

- By Type: IFE Hardware (largest share), IFE Connectivity (fastest growing)

- By IFE Connectivity: Satellite Connectivity (leading), Air-to-Ground Connectivity (fastest growing, CAGR of 20.5%)

- By Platform: Wide-Body Aircraft (largest share), Narrow-Body Aircraft (fastest growing, CAGR of 16.8%)

- By Region: North America leads; Asia Pacific is a key growth engine, accounting for over 37% of global passenger traffic.

Key Drivers

- Rising passenger expectations for personalized, on-demand digital content across devices.

- Advancements in satellite connectivity, including LEO and GEO constellations, enabling high-speed real-time streaming.

- Growing airline investment in bring-your-own-device (BYOD) wireless streaming to reduce hardware weight and cost.

Key Players

Panasonic Avionics Corporation, Thales Group, Collins Aerospace (RTX Corporation), Safran Passenger Innovations, Viasat Inc., Intelsat S.A., Gogo Inc., Lufthansa Systems GmbH & Co. KG, Burrana Pty Ltd., Astronics Corporation, Global Eagle Entertainment Inc. (Anuvu), Honeywell International Inc.

Global In-Flight Entertainment Market Size

The Global In-Flight Entertainment Market is projected to grow from USD 9.89 billion in 2025 to USD 10.88 billion in 2026 and reach USD 23.32 billion by 2034, registering a CAGR of 10% during the forecast period from 2026 to 2034.

The in-flight entertainment is a diverse array of digital and physical media systems designed to enhance the passenger experience during air travel. This domain includes seatback screens, wireless streaming platforms, audio systems, and interactive content delivery networks that provide movies, television series, music, games, and live connectivity. As global aviation recovers from recent disruptions, airlines are increasingly viewing entertainment not merely as an amenity but as a critical differentiator in a competitive landscape. According to the International Air Transport Association (IATA), global passenger numbers crossed an unprecedented milestone to reach 5.2 billion in 2025, forcing airlines to closely manage capacity constraints and find novel digital avenues to maintain high-quality customer retention. Research shows that international long-haul airline routes frequently surpass an 8-hour block time duration, making the integration of reliable, high-bandwidth In-Flight Entertainment and Connectivity (IFEC) suites a core requirement for ensuring passenger satisfaction. As per the Airports Council International (ACI) Europe, European airports welcomed a record 2.6 billion passengers in 2025, while global passenger experience studies from organizations like Apex demonstrate that interactive seatback technology remains a primary differentiator in airline brand selection. The shift towards personalized content consumption has driven airlines to adopt bring your own device strategies, allowing passengers to stream content directly to their smartphones and tablets.

Furthermore, the integration of high-speed satellite connectivity enables real-time streaming and social media access, transforming the cabin into a connected workspace. The market is thus characterized by a transition from static pre-loaded libraries to dynamic cloud-based content ecosystems that offer greater variety and immediacy. This evolution reflects broader consumer expectations for seamless digital experiences, compelling airlines to invest heavily in advanced hardware and software solutions to meet the demands of modern travelers.

MARKET DRIVERS

Rising Passenger Expectations for Personalized Digital Experiences

The escalating demand for personalized and on-demand digital content contributes to the growth of the in-flight entertainment market. This compels airlines to move beyond traditional broadcast models. Modern travelers, accustomed to the curated algorithms of streaming services like Netflix and Spotify, expect similar levels of customization and choice while airborne. Moreover, the Airline Passenger Experience Association (APEX) shows that a vast majority of long-haul travelers prioritize content variety, driving global network carriers to continuously expand their digital seatback catalogs with cloud-managed, multilingual entertainment libraries. The ability to pause, rewind, and resume content across devices enhances user control and satisfaction. Studies indicate that near-universal personal electronic device (PED) ownership among business and frequent travelers has allowed airlines to rapidly scale low-weight, browser-based wireless streaming networks across short-haul fleets. This shift allows for more frequent content updates via cloud synchronization, ensuring that new releases are available shortly after their terrestrial debut. Airlines are leveraging data analytics to understand viewing preferences, tailoring recommendations to individual profiles and increasing engagement rates. The Airlines Electronic Engineering Committee (AEEC) states that ultralong-haul flights require localized, high-capacity solid-state drive (SSD) cabin servers to ensure smooth, uninterrupted content distribution to hundreds of concurrent users without reliance on continuous satellite links. Furthermore, business travelers require access to productivity tools and news feeds, blending entertainment with utility. This convergence of leisure and work needs forces carriers to offer comprehensive digital ecosystems that cater to diverse passenger segments, thereby driving sustained growth in the in-flight entertainment sector.

Advancements in Satellite Connectivity and Broadband Technology

Rapid advancements in satellite connectivity and broadband technology are also a critical driver for the in-flight entertainment market. This enables high-speed internet access and real-time content streaming at cruising altitudes. Traditional in-flight entertainment systems relied on pre-loaded hard drives, limiting content freshness and interactivity. However, the deployment of low-earth-orbit satellite constellations has revolutionized cabin connectivity, offering bandwidth speeds comparable to ground-based fiber optics. Studies show that the rapid launch of multi-orbit low-Earth orbit (LEO) and geostationary (GEO) constellations has exponentially multiplied globally available space-based broadband throughput, driving down the cost of real-time cabin video streaming. This technological leap allows airlines to offer live television, sports broadcasts, and interactive gaming, which were previously impossible due to latency issues. The ability to stream content directly from the internet reduces the need for physical media storage and simplifies content management logistics. Passengers can now access their personal subscription accounts, such as Amazon Prime or Disney Plus, directly through the aircraft portal, creating a familiar and convenient user experience. This integration enhances perceived value and encourages passengers to choose airlines that offer superior connectivity. Furthermore, improved bandwidth supports ancillary revenue streams through targeted advertising and e-commerce opportunities within the entertainment interface. The synergy between robust connectivity and advanced entertainment platforms creates a compelling value proposition, driving airlines to invest heavily in infrastructure upgrades to remain competitive in the digital age.

MARKET RESTRAINTS

High Capital Expenditure and Installation Costs

The substantial capital expenditure required to install and upgrade these systems is a major restraint on the global in-flight entertainment market. This is particularly true for legacy carriers operating older fleets. Retrofitting aircraft with modern seatback screens, wiring harnesses, and server racks involves significant downtime and labor costs, impacting airline profitability. Sources state that deep-cabin wide-body retrofits encompassing smart seatback screens, power units, and routing infrastructure represent multi-million-dollar capital investments per aircraft, heavily impacted by engineering downtime. For airlines with large fleets, these costs accumulate rapidly, creating a financial barrier to widespread adoption. Additionally, the added weight of hardware components increases fuel consumption, contradicting sustainability goals and raising operational expenses. The rapid pace of technological obsolescence means that systems may become outdated within five years, necessitating further upgrades before the return on investment is fully realized. Smaller regional carriers and low-cost operators often lack the financial resources to compete with full-service airlines in this domain, leading to a disparity in service quality. Budget constraints force many airlines to prioritize essential safety and maintenance upgrades over entertainment enhancements, slowing market penetration. High capital requirements continue to hinder the rapid modernization of in-flight entertainment (IFE) systems across the global aviation industry. This barrier will persist until financing models become more flexible or hardware costs decrease significantly.

Content Licensing Complexities and Regional Restrictions

Complex content licensing agreements and regional copyright restrictions are significant obstacles to the in-flight entertainment market. This limits the availability and diversity of media offerings. Securing global rights for movies, television shows, and music is an intricate legal process involving multiple studios, distributors, and territorial jurisdictions. Research confirms that acquiring international airline exhibition windows requires navigating complex non-theatrical licensing frameworks, which frequently differ from domestic terrestrial streaming availability timelines. This fragmentation results in inconsistent content libraries across different routes and airlines, frustrating passengers who expect uniform access. These technical safeguards add complexity to the software architecture and can lead to user experience issues if not managed correctly.

Furthermore, the cost of licensing premium content continues to rise, squeezing margins for airlines already facing high operational costs. Independent filmmakers and smaller studios often lack the resources to navigate these complex licensing frameworks, reducing the diversity of independent and niche content available onboard. The administrative burden of tracking usage rights and ensuring compliance with evolving international laws diverts resources from innovation and customer service improvements. Content restrictions remain a persistent challenge that limits the potential of in-flight entertainment platforms to offer truly universal media libraries. This will continue until a standardized global licensing framework is established or digital rights management innovations simplify the process.

MARKET OPPORTUNITIES

Integration of Augmented Reality and Virtual Reality Technologies

The integration of augmented reality and virtual reality technologies unlocks potential for the in-flight entertainment market. This offers immersive experiences that transcend traditional screen boundaries. As headset technology becomes lighter and more affordable, airlines can provide passengers with virtual tours, interactive games, and 360-degree cinematic experiences without occupying additional cabin space. A study indicates that consumer adoption of standalone virtual reality (VR) and spatial computing headsets continues to steadily rise, establishing a baseline of user familiarity that airlines are leveraging to design immersive cabin applications. Airlines can partner with content creators to develop exclusive immersive experiences that highlight destination cultures or offer educational content, enhancing the overall travel narrative. Offering immersive spatial headsets on long-haul routes yields strong positive engagement, paving the way for premium-tier entertainment upgrades. This technology also offers solutions for space-constrained cabins, as it eliminates the need for bulky seatback installations. Furthermore, augmented reality applications can overlay information about flight status, meal options, or duty-free products onto the passenger view, creating interactive engagement opportunities. The ability to personalize visual environments helps reduce travel anxiety and improves comfort during extended flights. Technology providers are developing hygiene-friendly headset designs and easy sanitization protocols to address health concerns, making adoption more viable for commercial carriers. Airlines can differentiate their brand and attract tech-savvy travelers by embracing these emerging technologies. This opens new revenue streams through premium immersive content packages for those seeking novel ways to pass the time.

Expansion of Ancillary Revenue Through Targeted Advertising

The expansion of ancillary revenue through targeted advertising and e-commerce integration within in-flight entertainment platforms offers a lucrative opportunity for airlines to offset operational costs, which is expected to drive the growth of the global market. Modern digital interfaces allow for precise audience segmentation based on passenger profiles, travel history, and real-time behavior, enabling highly relevant ad placements. Airlines can partner with retail brands, hotels, and tourism boards to display interactive advertisements that allow passengers to make purchases or bookings directly through the entertainment system. The ability to track click-through rates and conversion metrics provides valuable data for optimizing marketing campaigns and maximizing return on investment. Furthermore, sponsored content and branded entertainment experiences offer subtle yet effective promotional opportunities that do not disrupt the user experience. The shift towards wireless streaming enables dynamic ad insertion, allowing airlines to update promotions in real time based on flight route and destination. This monetization model transforms the entertainment system from a cost center into a profit generator, encouraging further investment in platform development and content acquisition. Transparent data usage policies will be essential to maintain passenger trust as privacy regulations evolve. Thus, organizations can safely leverage these commercial opportunities.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns

Cybersecurity threats and data privacy concerns are major challenges to the in-flight entertainment market. This is because interconnected systems are becoming vulnerable to hacking and data breaches. Modern entertainment platforms are integrated with aircraft communication networks, creating potential entry points for malicious actors seeking to disrupt operations or steal passenger information. A successful breach could compromise sensitive personal data such as payment details and travel itineraries stored in user profiles, leading to severe reputational damage and legal liabilities. The complexity of securing heterogeneous systems from multiple vendors further complicates cybersecurity efforts, as inconsistencies in protocols create weaknesses. Additionally, the use of bring your own device strategies introduces risks related to malware transmission from personal gadgets to the aircraft network. Ensuring the resilience of entertainment systems against evolving cyber threats requires continuous investment in security audits, staff training, and software patches. The balance between seamless connectivity and strict security protocols remains delicate, with any perceived vulnerability potentially eroding passenger trust. These risks will remain a persistent challenge until comprehensive global cybersecurity standards for in-flight entertainment are established and uniformly implemented. Consequently, this could potentially hinder the adoption of advanced connected features.

Hardware Maintenance and Reliability Issues

Frequent hardware failures and high maintenance requirements are a major hurdle for the in-flight entertainment market. This impacts operational efficiency and passenger satisfaction. Seatback screens, touch panels, and audio jacks are subject to intense physical wear and tear from thousands of passengers annually, leading to malfunctions and broken components. Repairing or replacing faulty units often requires specialized technicians and spare parts, causing aircraft grounding or delayed departures if issues are not resolved quickly. The logistical challenge of managing inventory for diverse aircraft types and system generations further complicates maintenance operations. Wireless systems, while reducing physical hardware risks, introduce connectivity issues such as signal interference and server overload, which can degrade streaming quality and frustrate users. The rapid evolution of technology means that older hardware becomes incompatible with new software updates, forcing premature replacements. Ensuring consistent reliability across entire fleets requires rigorous testing and quality control measures, which increase upfront costs. Until more durable and self-diagnosing hardware solutions are developed, maintenance burdens will continue to affect the profitability and operational smoothness of in-flight entertainment services. Therefore, this necessitates constant vigilance and resource allocation from airline engineering teams.

REPORT COVERAGE

REPORT METRIC | DETAILS |

Market Size Available | 2025 to 2034 |

Base Year | 2025 |

Forecast Period | 2026 to 2034 |

Segments Covered | By Type, IFE Connectivity, Platform, and Region |

Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

Countries Covered | North AmericaEuropeAsia PacificLatin AmericaMiddle East and Africa |

Market Leaders Profiled | Panasonic Avionics Corporation, Thales Group, Collins Aerospace (RTX Corporation), Safran Passenger Innovations, Viasat, Inc., Intelsat S.A., Gogo Inc., Lufthansa Systems GmbH & Co. KG, Burrana Pty Ltd., Astronics Corporation, Global Eagle Entertainment Inc. (Anuvu), Honeywell International Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The IFE hardware segment dominated the in-flight entertainment market and accounted for a substantial share in 2025. This dominance of the segment was driven by the continued preference of full-service carriers for embedded systems that offer a premium and controlled user experience. Extensive infrastructure is required for seatback screens, audio systems, and onboard servers. According to sources, the vast majority of wide-body aircraft configured for long-haul routes feature built-in seatback screens, while International Air Transport Association (IATA) traffic data shows an accelerating airline industry trend toward “premiumisation” and cabin upgrades to enhance the passenger experience. The Federal Aviation Administration mandates strict safety certifications for all installed cabin equipment, ensuring that only robust and reliable hardware enters the market, which sustains revenue for established manufacturers. As per research, structural cabin systems are designed to last over a decade, prompting airlines to coordinate major IFE hardware retrofits alongside scheduled mid-life heavy maintenance checks. The integration of larger 4K displays and touch-sensitive interfaces has increased the unit cost of hardware, further bolstering the segment’s value share. Additionally, the need for powerful onboard servers to store vast content libraries requires significant physical space and cooling systems, adding to the hardware footprint. Airlines prioritize hardware reliability to minimize maintenance downtime, leading to substantial investments in durable components. The tactile nature of hardware makes it the primary interface for passengers, ensuring its central role in the entertainment ecosystem despite the rise of wireless alternatives. Consequently, the hardware segment remains the largest contributor to market revenue, supported by continuous fleet modernization and the installation of next-generation displays in new aircraft deliveries.

On the contrary, the IFE connectivity segment is expected to exhibit a noteworthy CAGR of 18.2% from 2026 to 2034. This rapid growth of the segment is fueled by the increasing passenger demand for real-time internet access and the ability to stream personal content from cloud-based services. According to research, global airborne high-speed data capacity is expanding rapidly due to the deployment of new Geostationary (GEO) and Low Earth Orbit (LEO) satellite constellations, driving down latency for airline passengers. The shift towards bring your own device strategies allows airlines to reduce hardware weight while offering unlimited content choices through streaming platforms. As per surveys, a significant majority of travelers prefer using their personal electronic devices (BYOD) for connectivity, prompting airlines to deploy high-speed, Next-Gen Wi-Fi networks and streaming gateways. The deployment of low-Earth-orbit satellite constellations has revolutionized connectivity, making live video streaming and video conferencing feasible at cruising altitudes. This technological advancement transforms the cabin into a connected workspace, appealing to business travelers who require constant connectivity.

Furthermore, connectivity enables dynamic content updates and targeted advertising, creating new revenue streams for airlines. The scalability of wireless solutions allows for easier retrofitting of older fleets compared to heavy hardware installations. These factors collectively position IFE connectivity as the most dynamic and rapidly expanding segment in the market.

By IFE Connectivity Insights

The satellite connectivity segment led the global market and captured a significant share in 2025. This leading position of the segment was attributed to the increasing number of long-haul international flights that require uninterrupted internet access for passengers and crew. Satellite connectivity provides global coverage, including over oceanic and remote regions where ground-based signals are unavailable. According to Viasat (formerly Inmarsat), satellite networks remain indispensable for long-haul routes, with the vast majority of aircraft crossing oceans relying on geostationary satellite constellations for essential safety, operation, and cabin broadband communications. A study highlights that modern Ku-band and Ka-band satellites offer bandwidth speeds exceeding 100 Mbps per aircraft, supporting multiple simultaneous high-definition video streams. As per the International Air Transport Association (IATA) passenger insights, modern travelers increasingly demand seamless gate-to-gate digital connectivity, prompting major airlines to prioritize high-capacity satellite upgrades across their long-haul fleets. The reliability of satellite links ensures consistent performance regardless of terrain, making it the preferred choice for global operators. Additionally, the expansion of geostationary satellite fleets has reduced costs and improved service availability, encouraging wider adoption among mid-tier airlines. The ability to support critical operational data transmission alongside passenger entertainment further solidifies the segment’s leadership. Regulatory support for spectrum allocation and international cooperation on satellite standards facilitate smooth operations across borders. These technical advantages and widespread availability ensure that satellite connectivity remains the backbone of global in-flight internet services, driving sustained investment and market dominance.

However, the air-to-ground connectivity segment is predicted to witness the highest CAGR of 20.5% during the forecast period due to its cost-effectiveness and high-speed performance for domestic and regional routes. This growth is also propelled by the deployment of advanced 4G and 5G terrestrial networks that offer lower latency and higher bandwidth compared to traditional satellite systems for short- to medium-haul flights. According to sources, next-generation Air-to-Ground (ATG) networks can deliver high-speed broadband to aircraft, serving as a reliable option for text, browsing, and entertainment on domestic short-haul flights. The International Telecommunication Union notes that the expansion of cellular tower infrastructure along major flight corridors has significantly improved coverage reliability, making this technology viable for busy domestic markets. As per research, the expansion of dedicated ground-based cell towers optimized for aviation has significantly enhanced connectivity uptime and reliability across high-density domestic flight paths. The simplicity of the technology allows for easier maintenance and quicker upgrades as terrestrial networks evolve. Airlines operating primarily within continental boundaries, such as those in North America and Europe, are increasingly adopting this solution to enhance customer satisfaction on high-frequency routes. The ability to leverage existing telecommunications infrastructure reduces capital expenditure, accelerating adoption rates. These economic and technical benefits position air-to-ground connectivity as the fastest-growing segment, particularly in regions with dense network coverage.

By Platform Insights

In 2025, the wide-body aircraft segment held the majority share of the in-flight entertainment market because of the long duration of flights and the premium service expectations associated with these aircraft. Wide-body planes such as the Boeing 787 and Airbus A350 typically operate on intercontinental routes lasting 8 to 15 hours, necessitating comprehensive entertainment systems to keep passengers engaged. According to airline fleet statistics tracked by IATA Economics, wide-body aircraft dominate high-capacity transoceanic corridors, justifying substantial capital investments in luxury cabin hardware to stay competitive. As per sources, travelers on long-haul international flights spend a substantial portion of their journey interacting directly with cabin entertainment systems, cementing IFE as a critical touchpoint for airline brand loyalty. According to airline cabin configuration and product design standards, wide-body aircraft feature immersive entertainment upgrades, high-definition screens, and expansive content suites to satisfy corporate and premium leisure travelers. The complex wiring and server infrastructure required for these large cabins contribute to higher per-unit revenue for IFE providers. Airlines prioritize state-of-the-art hardware and connectivity on these fleets to differentiate their brand and attract business class passengers. The high utilization rates of wide-body aircraft on busy international routes ensure frequent wear and tear, driving regular maintenance and upgrade cycles. Furthermore, the introduction of new wide-body models with integrated digital ecosystems creates opportunities for suppliers to install next-generation systems. These factors collectively sustain the dominance of the wide-body segment in the global IFE market.

But the narrow-body aircraft segment is anticipated to witness the fastest CAGR of 16.8% between 2026 and 2034 owing to the massive volume of short- to medium-haul flights and the rising adoption of wireless streaming solutions. This expansion is also fuelled by the expansion of low-cost carriers and regional airlines that operate high-frequency domestic routes, where traditional seatback screens are often omitted to save weight and cost. According to a study, single-aisle narrow-body aircraft represent over 75% of the total global fleet, forming an expansive market for lightweight, scalable IFE architectures. According to sources, the average stage length for narrow-body routes falls well below 3 hours, making wireless Bring-Your-Own-Device (BYOD) streaming an operationally efficient and lightweight alternative to heavy seatback hardware. This approach significantly reduces installation costs and maintenance burdens, making it economically viable for high-volume operators. The increasing demand for connectivity even on short flights drives airlines to invest in robust Wi Fi infrastructure. Furthermore, the retrofitting of older narrow-body fleets with modern wireless systems offers significant growth opportunities for IFE providers. The scalability and flexibility of wireless solutions align perfectly with the operational model of narrow-body carriers, positioning this segment for rapid expansion in the coming years.

COUNTRY LEVEL ANALYSIS

North America Flight Entertainment Market Analysis

North America was the top performer in the global in-flight entertainment market and occupied a commanding share in 2025. This prominence of the market was driven by a mature aviation infrastructure and a strong presence of major technology providers specializing in IFE solutions. The regional market is known for high adoption rates of advanced connectivity and wireless streaming technologies. According to the FAA Aerospace Forecasts, the United States operates a massively growing domestic airline infrastructure, while independent connectivity analysts like Valour Consultancy note that North American carriers lead global retrofits for high-speed, satellite-powered cabin Wi-Fi networks. The Airline Passenger Experience Association (APEX) shows that North American travelers show an overwhelming preference for gate-to-gate touchless internet access, prompting major network carriers to invest heavily in multi-orbit satellite solutions. Also, the Consumer Technology Association (CTA) notes near-universal smartphone ownership among adults, a baseline metric that has allowed regional low-cost carriers to entirely drop heavy seatback screens in favor of streaming portals to passenger personal devices. Major US carriers have led the industry in partnering with satellite providers to offer free or subsidized connectivity, setting a benchmark for customer expectations. The competitive landscape among domestic airlines forces continuous innovation in content offerings and user interface design. Additionally, the presence of key IFE manufacturers and software developers in the region fosters rapid technological advancements and integration. Regulatory support for spectrum allocation and cybersecurity standards ensures a stable environment for market growth. These factors collectively sustain North America’s leadership, with ongoing investments in 5Gair-to-groundd systems and personalized digital services driving further expansion.

Europe Flight Entertainment Market Analysis

Europe was the next prominent region in the global in-flight entertainment market due to stringent regulatory standards and a focus on sustainable and efficient cabin solutions. The region is home to major aircraft manufacturers and airlines that prioritize passenger comfort and environmental responsibility in their IFE strategies. Studies from the International Civil Aviation Organization (ICAO) outline weight reduction as a core lever for hitting net-zero targets, prompting European operators to actively substitute legacy copper-wired hardware with lightweight wireless server nodes. Eurostat outlines a steady upward trajectory in general mobile e-commerce use, and commercial aviation consumer reports indicate that airlines leverage this digital adoption by introducing pre-flight application syncs to streamline overall passenger digital identity and entertainment options. The General Data Protection Regulation imposes strict rules on data privacy, influencing how airlines collect and use passenger viewing data for personalization. Collaborative initiatives among European airlines aim to standardize connectivity protocols and content licensing agreements, simplifying cross-border operations. The presence of specialized IFE suppliers in countries like France and Germany supports innovation in hardware design and software integration. These regulatory and cultural factors shape a market that values efficiency, privacy, and high-quality user experiences, ensuring steady growth and technological refinement in the region.

Asia Pacific Flight Entertainment Market Analysis

The Asia Pacific region expands quickly in the in-flight entertainment market, fueled by rapid economic expansion and a burgeoning middle class with increasing travel propensity. Countries such as China, India, and Japan are investing heavily in fleet modernization and airport infrastructure to accommodate rising passenger numbers. According to the International Air Transport Association (IATA), the Asia-Pacific region stands as the world’s largest aviation market, accounting for over 37% of global passenger traffic and driving massive regional demand for next-generation In-Flight Entertainment (IFE) retrofits. The Airline Passenger Experience Association (APEX) shows that major Chinese network carriers are aggressively outfitting their wide-body fleets with 4K resolution seatback screens and high-speed satellite connectivity to capture premium passenger market share on competitive long-haul international routes. India’s Ministry of Civil Aviation indicates that the regional connectivity scheme (UDAN) has accelerated the induction of narrow-body and regional aircraft, creating a highly specific opportunity for technology vendors to install lightweight, cost-effective, browser-based wireless streaming portals rather than heavy hardware. The young and tech-savvy population in the region exhibits high demand for digital entertainment and social media access during flights. Local partnerships between international IFE vendors and domestic airlines facilitate customization of content to suit regional preferences and languages. The growth of low-cost carriers in Southeast Asia also drives the adoption of cost-effective wireless streaming solutions. These dynamics position Asia Pacific as a critical growth engine, with substantial potential for expansion as awareness and affordability improve across the continent.

Latin America Flight Entertainment Market Analysis

Latin America grew steadily in the global in-flight entertainment market owing to gradual modernization and increasing focus on customer experience differentiation. The region relies heavily on narrow-body aircraft for domestic and intra-regional flights, driving demand for lightweight and cost-effective IFE solutions. Also, the International Air Transport Association (IATA) notes that while airport infrastructure spending across Latin America continues to face capacity bottlenecks, regional airlines are independently financing interior cabin modernizations to remain competitive with international carriers. Brazil and Mexico are the largest markets in the region, with major airlines introducing wireless streaming services to enhance passenger engagement on short-haul routes. In addition, the International Air Transport Association (IATA) reveals that Latin American passenger traffic surged by 11.4% in 2025, fueled by a powerful rebound in international tourism and expanded transatlantic routing. The adoption of bring your own device models is gaining traction as airlines seek to minimize capital expenditure while offering diverse content options. Challenges related to currency fluctuations and budget constraints limit the widespread installation of expensive seatback hardware, favoring scalable wireless alternatives. Regional collaborations aim to harmonize content licensing and connectivity standards, facilitating smoother operations across borders. The growing awareness of digital amenities among travelers prompts airlines to prioritize IFE upgrades to remain competitive. While the market size is smaller compared to other regions, the growth potential is significant as economic stability improves and air travel becomes more accessible to the broader population.

Middle East and Africa Flight Entertainment Market Analysis

The Middle East and Africa region holds a notable position in the global in-flight entertainment market due to major hub carriers that set global benchmarks for luxury and technology. Gulf airlines operate some of the most advanced fleets in the world, featuring cutting-edge IFE systems with large, high-resolution screens and extensive content libraries. Annual metrics from the International Air Transport Association (IATA) show that Middle Eastern carriers transported more than 230 million passengers in 2025, utilizing their strategic geographic hubs to anchor long-haul, wide-body fleets equipped with high-end, premium entertainment ecosystems. The General Civil Aviation Authority in the United Arab Emirates encourages innovation in cabin services, prompting airlines to invest in the latest IFE technologies to maintain their competitive edge. The harsh environmental conditions in some parts of the region require durable and reliable hardware capable of withstanding extreme temperatures. Partnerships with global content providers ensure that passengers have access to a wide variety of international and regional media. The focus on premium service and brand differentiation drives continuous upgrades in both hardware and software platforms. The growth of air cargo and business travel also contributes to demand for high-quality entertainment and connectivity solutions. These factors collectively support steady market growth, with a focus on delivering world-class passenger experiences through advanced technological integration.

COMPETITIVE LANDSCAPE

The competition in the in-flight entertainment market is intense and characterized by rapid technological advancements and a few dominant global players. Major companies compete based on system reliability, content variety,y and connectivity speed. Innovation in wireless streaming and satellite integration serves as a key differentiator for suppliers seeking to attract airline contracts. Companies strive to offer lightweight and energy-efficient solutions that align with sustainability goals. Strategic partnerships with content providers and telecommunications firms are crucial for delivering comprehensive entertainment packages. Price competition is moderate as airlines prioritize quality and passenger satisfaction over initial cost savings. The market sees frequent launches of new software platforms featuring artificial intelligence and personalized user experiences. Geographic expansion into emerging markets offers significant growth opportunities but requires adaptation to local content preferences. Regulatory compliance regarding data privacy and safety standards influences competitive dynamics. Mergers and acquisitions are common strategies used to consolidate technology portfolios and expand service capabilities. Overall, the landscape is shaped by a balance of technological leadership, customer-centric innovation, and operational efficiency among key participants who aim to transform the cabin into a connected digital environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominant role in the Global In-Flight Entertainment Market include

- Panasonic Avionics Corporation

- Thales Group

- Collins Aerospace (RTX Corporation)

- Safran Passenger Innovations

- Viasat, Inc.

- Intelsat S.A.

- Gogo Inc.

- Lufthansa Systems GmbH & Co. KG

- Burrana Pty Ltd.

- Astronics Corporation

- Global Eagle Entertainment Inc. (Anuvu)

- Honeywell International Inc.

TOP LEADING PLAYERS IN THE MARKET

- Thales Group is a global leader in providing comprehensive in-flight entertainment and connectivity solutions for commercial aviation. The company specializes in advanced seatback systems, wireless streaming platforms, and high-speed satellite connectivity services. Thales recently launched its next-generation Avionics 2020 suite, which integrates artificial intelligence to personalize passenger content recommendations. This innovation enhances user engagement and streamlines cabin operations for airlines. The company actively collaborates with major airframers to ensure seamless integration of IFE systems into new aircraft designs. Thales also focuses on cybersecurity measures to protect passenger data and aircraft networks from digital threats. By expanding its global service network, Thales ensures timely maintenance and support for airline customers worldwide. These strategic initiatives reinforce its position as a trusted partner for airlines seeking to deliver superior digital experiences and operational efficiency in the modern aviation landscape.

- Panasonic Avionics Corporation delivers innovativein-flightt entertainment and connectivity technologies tailored for the global aviation industry. The company offers a wide range of solutions, including high-definition video systems, live television streaming, and robust Wi Fi networks. Panasonic recently introduced its XSeries platform,m which features modular hardware and cloud-based content management capabilities. This flexibility allows airlines to customize entertainment offerings and update libraries in real time without physical media swaps. The company partners with leading content providers to secure exclusive rights for popular movies and series. Panasonic also invests heavily in research and development to reduce system weight and power consumption. Its commitment to sustainability aligns with airline goals to lower carbon emissions. By focusing on reliability and user experience, Panasonic strengthens its market presence and supports airlines in meeting evolving passenger expectations for connected and immersive travel experiences.

- Collins Aerospace provides advanced in-flight entertainment systems that combine hardware durability with sophisticated software interfaces. The company serves a broad spectrum of aircraft types with scalable solutions ranging from basic audio systems to complex 4K video networks. Collins Aerospace recently expanded its connectivity portfolio by integrating low-Earth-orbit satellite technologies for faster internet speeds. This enhancement enables passengers to stream high-quality video and participate in video calls during flights. The company emphasizes interoperability, allowing its systems to work seamlessly with various airline operational platforms. Collins Aerospace also offers comprehensive maintenance programs that utilize predictive analytics to minimize downtime. By leveraging its extensive aerospace expertise,e the company ensures high reliability and safety standards. These efforts help airlines improve customer satisfaction and operational efficiency while reducing total cost of ownership through innovative and durable entertainment solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the thin-flight entertainment market primarily focus on technological innovation and strategic partnerships to enhance the passenger experience. Companies invest heavily in developing lightweight wireless streaming solutions to reduce aircraft weight and fuel consumption. Integration of artificial intelligence enables personalized content recommendations and improved user interfaces. Strategic collaborations with satellite providers ensure high-speed global connectivity for real-time streaming. Partnerships with content studios secure exclusive media rights and diverse library options. Expansion of cloud-based platforms facilitates easy content updates and remote management. Emphasis on cybersecurity protects passenger data and aircraft systems from digital threats. Adoption of modular hardware designs allows for flexible upgrades and easier maintenance. These strategies collectively drive market growth and help airlines differentiate their services in a competitive industry.

MARKET SEGMENTATION

This research report on the global In-Flight Entertainment Market is segmented and sub-segmented into the following categories.

By Type

- IFE Hardware

- IFE Connectivity

By IFE Connectivity

- Satellite Connectivity

- Air-to-Ground Connectivity

By Platform

- Wide-Body Aircraft

- Narrow-Body Aircraft

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source www.marketdataforecast.com ’