Flutter Entertainment has had a tough run over the past year, with the stock down 61.9%, yet current valuation checks still flag it as looking cheap against its fundamentals. High profile interest from investors such as Michael Burry has sharpened the focus on whether the market has pushed Flutter too far to the downside or is correctly pricing in regulatory and competitive risks.

- Over the last 12 months, Flutter Entertainment’s share price has fallen 61.9%, which puts recent interest from high profile investors against a backdrop of heavy losses for existing shareholders.

- On the positive side, renewed attention on regulated sportsbook operators, including Burry’s long position, can support sentiment, while potential tightening of gambling affordability checks and wider regulatory scrutiny may weigh on how much value the market is willing to ascribe to future earnings.

- Across Simply Wall St’s valuation framework, Flutter Entertainment screens as undervalued on 5 of 6 checks, suggesting the broader set of metrics leans cheap rather than expensive for the current price 5/6.

The issue now is whether Flutter Entertainment’s current share price already reflects these regulatory and competitive risks, or if the valuation still provides a margin of safety for investors willing to accept them.

Find out why Flutter Entertainment’s -61.9% return over the last year is lagging behind its peers.

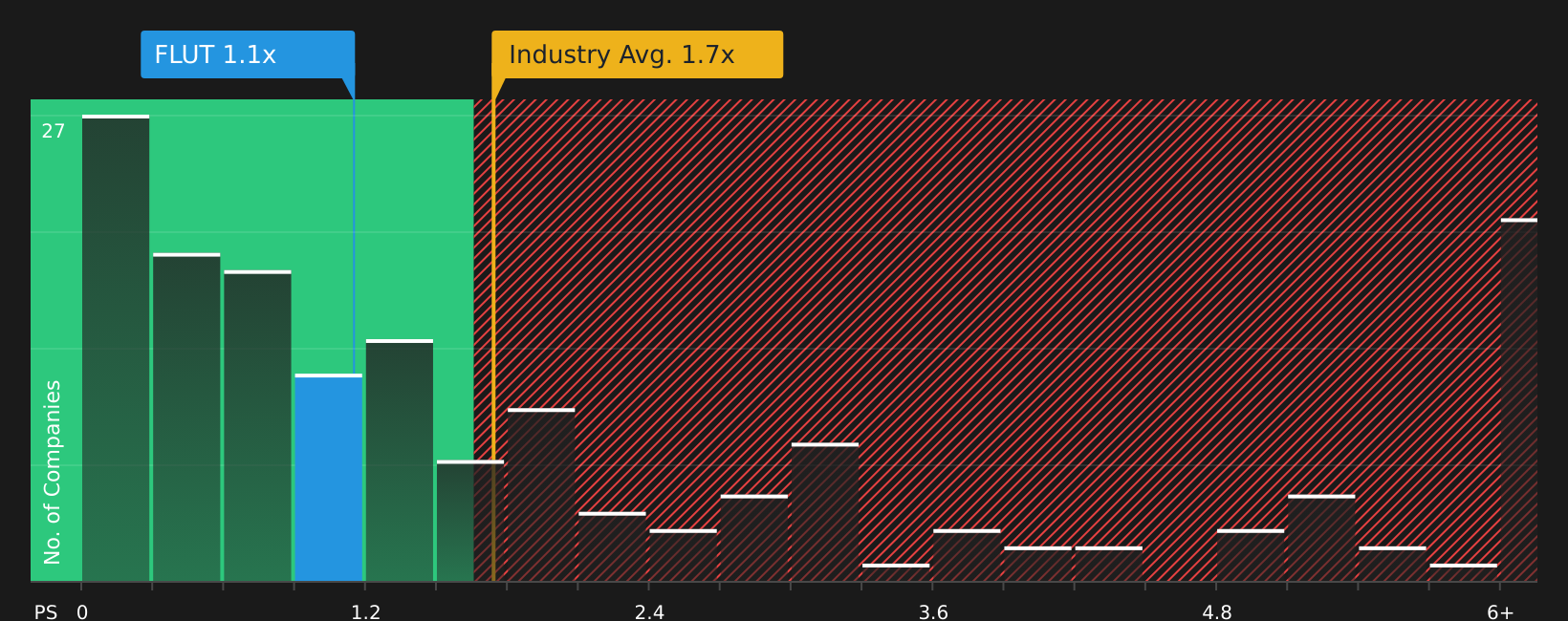

Is Flutter Entertainment Still Cheap on Sales?

P/S is a useful yardstick for Flutter Entertainment because revenue is a core focus for sportsbook investors and is less affected by near term earnings swings from marketing or product investment.

On this basis, Flutter Entertainment trades on a P/S of about 1.1x, compared with an industry average of roughly 1.7x and a peer group average around 1.6x. In other words, the stock is changing hands at a lower revenue multiple than many hospitality and betting peers, despite operating in the same broad sector. The Fair Ratio, which adjusts for the company’s growth profile, margins, scale and risk, sits higher at about 2.6x.

Because this gap is large, Flutter Entertainment screens as undervalued on sales even after the high profile interest and recent headlines around regulatory pressure on gambling affordability checks.

Overall, Flutter Entertainment appears undervalued on its P/S multiple relative to both peers and the tailored Fair Ratio benchmark.

See what the numbers say about this price — find out in our valuation breakdown.

The Flutter Entertainment Narrative: What Would Justify Today’s Price?

Simply Wall St Narratives for Flutter Entertainment pick up where the valuation work leaves off by spelling out what paths for Flutter Entertainment’s revenue growth, margins and earnings would need to play out for the current share price to look high, low or broadly fair. Instead of relying on a single multiple or model output, each narrative lays out the assumptions behind its view of fair value, so you can compare those inputs with Flutter Entertainment’s reported results over time on the Community page.

Community views on Flutter Entertainment are split, with one camp seeing a reset opportunity while another focuses on execution and prediction market risks.

Bull case: 31% undervalued

“Product innovation particularly in live betting and personalized betting features (e.g., “Your Way Parlay,” Same Game Parlay Live, and platform migrations across Snai and FanDuel) positions Flutter to capture greater user engagement and wallet share, supporting both revenue growth and long-term margin expansion…”

Read the full Bull Case to see why Flutter Entertainment could be undervalued

Bear case: 41% overvalued

“Despite FanDuel’s scale leadership in U.S. Sportsbook and an improving product mix in NBA and parlays, persistently elevated promotional intensity and competitors’ willingness to spend uneconomically could structurally compress unit economics, limiting contribution margin and slowing the pace of earnings growth…”

Read the full Bear Case to see why Flutter Entertainment could be overvalued

Do you think there’s more to the story for Flutter Entertainment? Head over to our Community to see what others are saying!

The Bottom Line

Flutter Entertainment screens as undervalued on market multiples, with the P/S and Fair Ratio work pointing to a discount relative to sector peers. The high overall value score suggests that, on the data available, the stock still looks cheap rather than fully priced. The key question is whether that discount reflects a genuine margin of safety or a lasting penalty for regulatory pressure and intense competition. For now, the crux of the Flutter Entertainment debate is whether the business can sustain attractive economics in the face of tighter gambling rules and aggressive rivals, which will ultimately decide if the current valuation proves appealing or a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’