AMC Entertainment Holdings stock now trades around US$1.94 after a long slide in which shareholders have seen the value of their investment fall about 99% over five years, while some valuation checks still suggest the shares are not clearly expensive on current metrics.

- Over the past five years, AMC Entertainment Holdings has declined about 99%, which means any fresh move in the share price carries outsized importance for existing holders.

- Recent balance sheet moves to refinance high interest debt and convert some notes into equity can support equity value if interest costs ease, but the company still carries meaningful net debt that may keep the risk of further capital raising on the table.

- On Simply Wall St’s broader valuation checks, AMC Entertainment Holdings screens as a mixed picture rather than a clear bargain or clear overvaluation, passing 3 of 6 tests, according to the 3 out of 6 valuation score.

The issue now is whether AMC Entertainment Holdings’ current price already reflects the progress on debt and box office expectations, or if the recent performance still leaves a margin between the share price and what investors are paying for the underlying business.

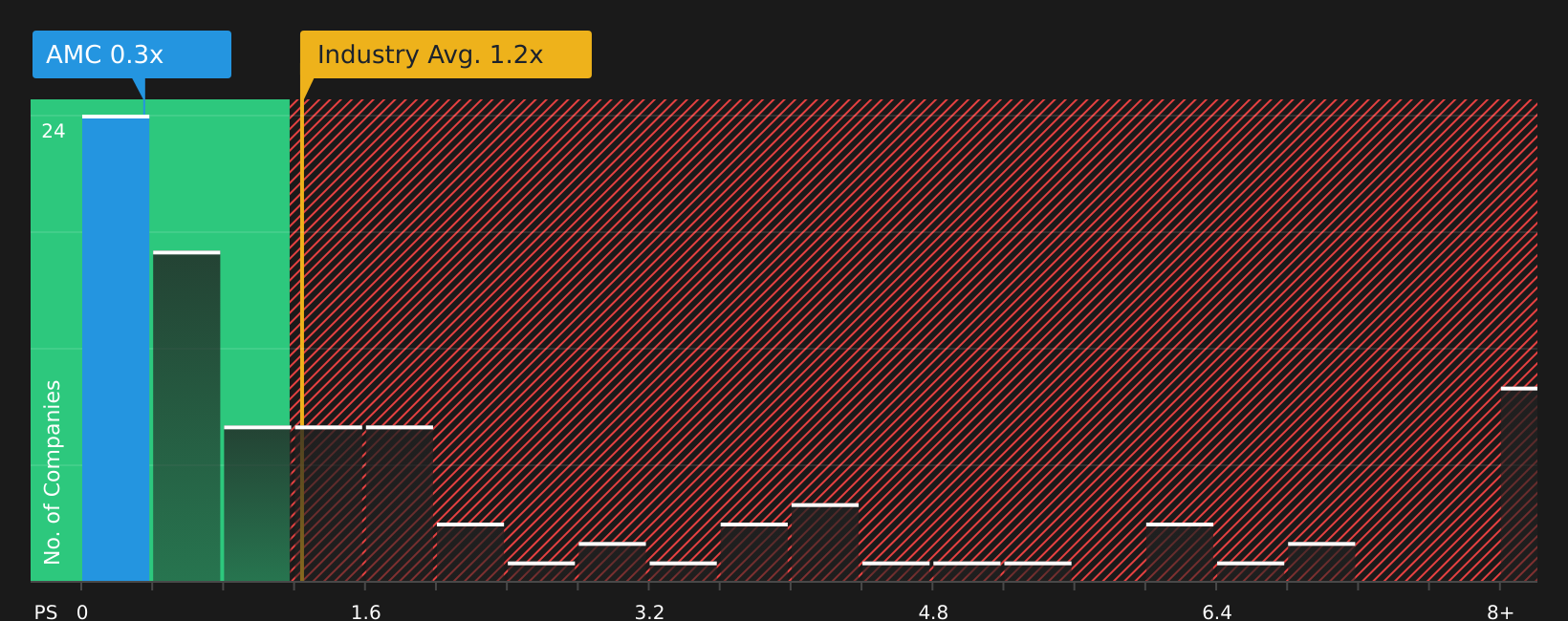

Is AMC Entertainment Holdings a Bargain on Sales?

The price-to-sales ratio suits AMC Entertainment Holdings because recent accounting losses mean earnings-based multiples such as P/E are less helpful. AMC stock trades on a P/S of about 0.3x, compared with an entertainment industry average of roughly 1.2x and a peer group average of about 2.8x, so investors are paying a much lower price for each dollar of AMC’s revenue than for many competitors.

On Simply Wall St’s tailored fair P/S estimate of about 0.7x, which reflects AMC Entertainment Holdings’ specific risks and financial profile, the current 0.3x level sits at a sizeable discount to what the model suggests could be reasonable. Despite the recent lift in sentiment after AMC’s debt refinancing and box office commentary, the stock still trades well below both the industry average and this fair ratio benchmark on a sales basis.

Overall, AMC Entertainment Holdings appears undervalued on the P/S multiple, with the shares trading at a sizable discount to both peers and the modelled fair level.

See what the numbers say about this price — find out in our valuation breakdown.

The AMC Entertainment Holdings Narrative: What Would Justify Today’s Price?

Simply Wall St Narratives pick up where the valuation puzzle around AMC Entertainment Holdings’ low P/S ratio leaves off by explaining which combinations of future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today’s price, and they sit on Simply Wall St’s Community page. Each Narrative treats AMC Entertainment Holdings’ fair value as a thesis about the business that can be tracked over time, rather than a one off snapshot.

The community is split between two very different scenarios for AMC Entertainment Holdings, with one side focused on premium cinema progress and the other on debt and cash flow pressure.

Bull case: 10% undervalued

“Ongoing success in diversifying content such as direct distribution of concerts (Taylor Swift, Beyoncé, Eminem), niche film events, and alternative content reduces dependence on studio box office releases and capitalizes on demand for event-based cinema…”

Read the full Bull Case to see why AMC Entertainment Holdings could be undervalued

Bear case: 62% overvalued

“AMC faces intensifying competition from streaming platforms and at-home entertainment, which continues to shift consumer behavior away from physical movie theaters…”

Read the full Bear Case to see why AMC Entertainment Holdings could be overvalued

Do you think there’s more to the story for AMC Entertainment Holdings? Head over to our Community to see what others are saying!

The Bottom Line

AMC Entertainment Holdings screens as undervalued on its P/S ratio, which points to a clear discount compared with many peers and with the tailored fair multiple discussed above. At the same time, the broader valuation checks are mixed rather than emphatically supportive, reflecting balance sheet leverage and the possibility of further capital needs. For investors, the key question is whether AMC’s low multiple compensates for those ongoing debt and cash flow pressures, or whether that discount is the market correctly pricing the risk that box office trends and premium formats do not translate into sustainably stronger economics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’