- Hasbro has signed a long term lease for new creative office space at The Lot at Formosa in West Hollywood.

- The move expands Hasbro’s presence at a historic Hollywood studio campus in the core of the entertainment production district.

- The new space is intended to support the company’s growing focus on branded entertainment and content related activities.

For investors watching NasdaqGS:HAS, the new lease lands at a time when the stock trades at $97.48, with returns of 3.7% over the past week, 7.8% over the past month, and 17.5% year to date. Over a longer horizon, the stock shows returns of 64.4% over 1 year, 83.2% over 3 years, and 24.7% over 5 years, which frames this Hollywood expansion against a backdrop of substantial multi year share price moves.

By committing to a creative hub in West Hollywood, Hasbro is placing more of its operations in the middle of film and television production activity. For shareholders, that location choice may be relevant to how the company builds out its entertainment pipeline, manages partnerships, and positions its branded content alongside established studios and production houses.

Stay updated on the most important news stories for Hasbro by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Hasbro.

2 things going right for Hasbro that this headline doesn’t cover.

Quick Assessment

- ✅ Price vs Analyst Target: At $97.48, Hasbro trades about 14% below the $113.73 analyst target, with the low end of the target range at $95 and the high at $125.

- ✅ Simply Wall St Valuation: Shares are assessed as trading roughly 62% below estimated fair value, which flags a valuation gap.

- ✅ Recent Momentum: The stock is up 7.8% over the past 30 days, suggesting short term positive sentiment.

There is only one way to know the right time to buy, sell or hold Hasbro. Head to the Simply Wall St

company report for the latest analysis of Hasbro’s Fair Value.

Key Considerations

- 📊 The new Hollywood lease ties directly into Hasbro’s push into branded entertainment, which could influence how investors think about its mix of toy and content revenues over time.

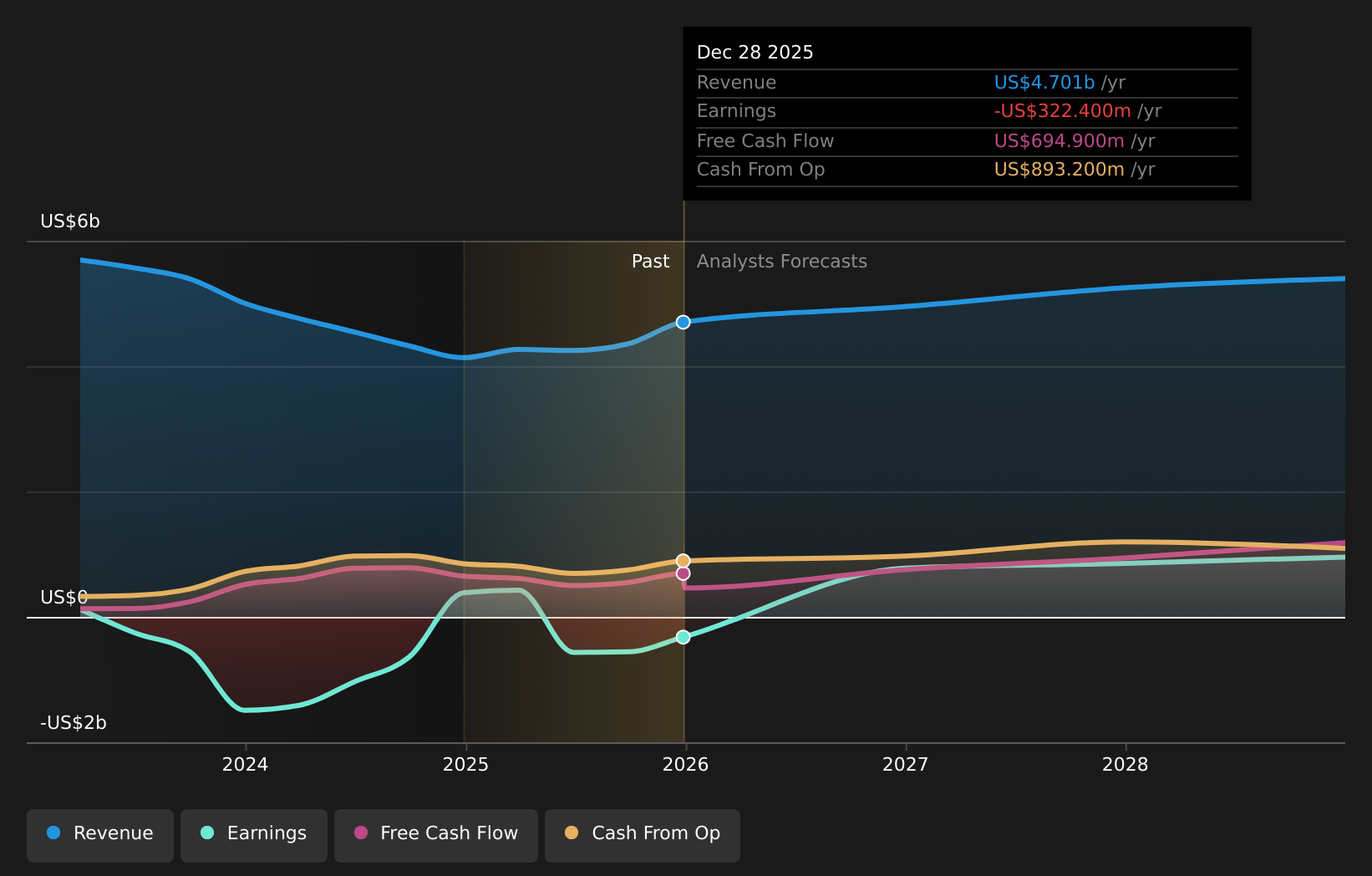

- 📊 Watch how content related spending, P/E relative to the industry average of 25.14, and progress against analyst earnings expectations line up with this expanded footprint.

- ⚠️ Key risks already flagged include a 2.87% dividend that is not well covered by earnings, a high debt load and recent insider selling.

Dig Deeper

For the full picture including more risks and rewards, check out the

complete Hasbro analysis. Alternatively, you can visit the

community page for Hasbro to see how other investors believe this latest news will impact the company’s narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hasbro might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’