- In June 2026, Caesars Entertainment Inc. announced that it had expanded its partnership with three Wabanaki Nations in Maine to cover online casino gaming, aiming to launch Caesars Palace Online Casino, Caesars Sportsbook & Casino and Horseshoe Online Casino in 2026, subject to regulatory approval and integrated with Caesars Rewards and a universal digital wallet.

- A distinctive element of this agreement is Caesars’ commitment to employ and train tribal members while providing financial support for community programs, tying digital gaming expansion directly to local economic and social benefits.

- We’ll now examine how this expanded tribal iGaming partnership, with its workforce and community commitments, might influence Caesars Entertainment’s broader investment narrative.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Caesars Entertainment Investment Narrative Recap

To own Caesars Entertainment today, you need to believe that its push into higher margin digital gaming can complement its physical casinos and help absorb ongoing debt and cost pressures. The expanded iGaming partnership in Maine fits that thesis by extending Caesars’ digital reach, but on its own it does not clearly change the near term catalysts around digital profitability or the key risk tied to leverage and capital needs.

The most relevant recent development alongside this Maine announcement is the pending Fertitta Entertainment acquisition, which includes Caesars’ US$11.9 billion debt load and would take the company private at US$31 per share. If completed, that deal could reshape how investors think about both the upside from digital initiatives like Maine and the downside from balance sheet risk, since the current public equity narrative would effectively be capped at the offer terms.

But alongside this digital expansion, investors should also be aware of the ongoing risk that Caesars’ substantial debt could start to matter much more if…

Read the full narrative on Caesars Entertainment (it’s free!)

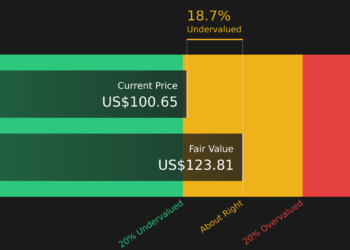

Caesars Entertainment’s narrative projects $12.6 billion revenue and $321.3 million earnings by 2029. This requires 3.0% yearly revenue growth and an $806.3 million earnings increase from -$485.0 million today.

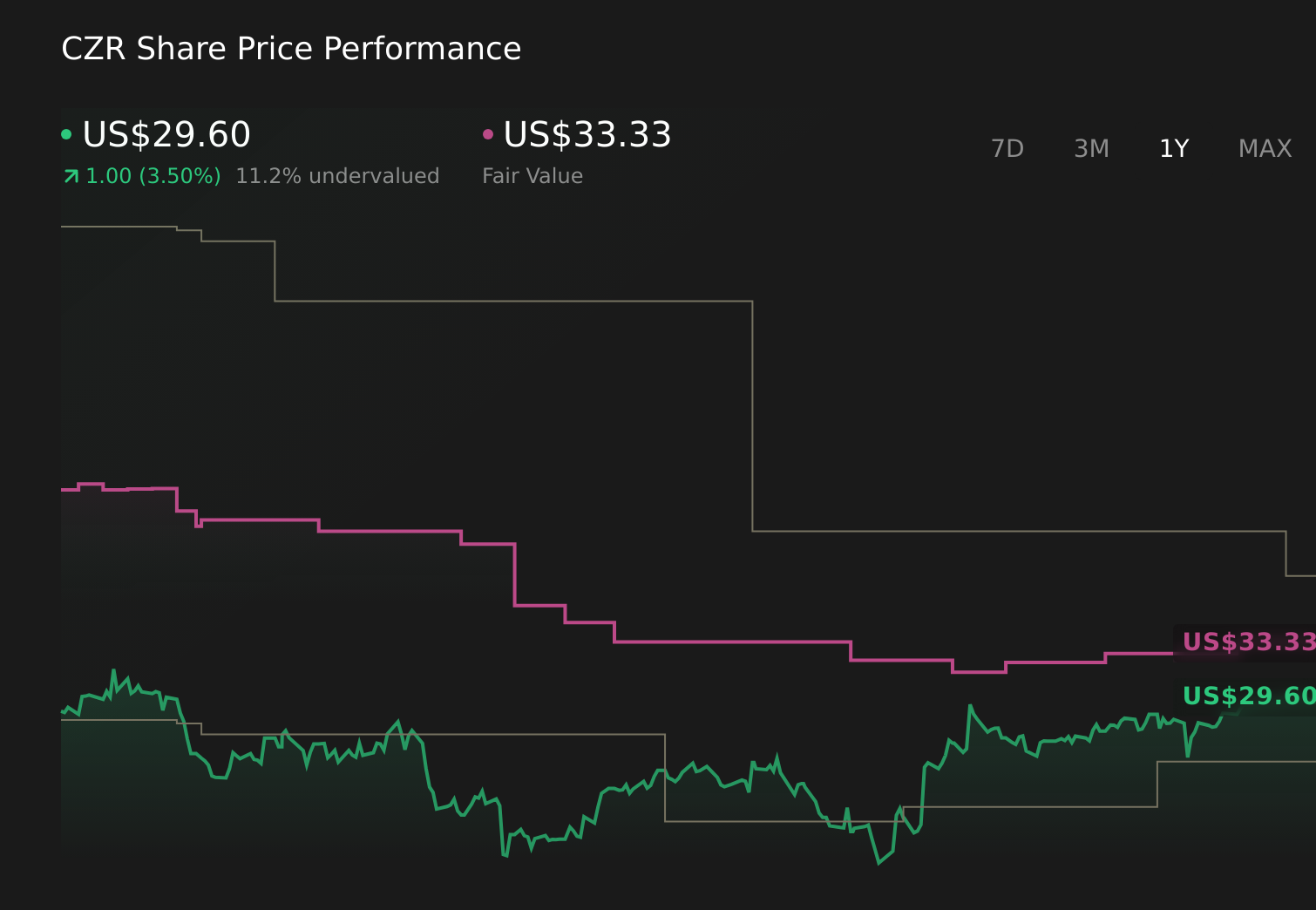

Uncover how Caesars Entertainment’s forecasts yield a $33.33 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some analysts were already optimistic, penciling in revenue of about US$13.4 billion and earnings of roughly US$611.7 million by 2029, while others highlight that Caesars’ heavy U.S. exposure could amplify any regulatory or economic shock, so this new tribal iGaming deal might eventually tilt expectations in either direction once everyone reassesses their assumptions.

Explore 3 other fair value estimates on Caesars Entertainment – why the stock might be worth just $33.33!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’