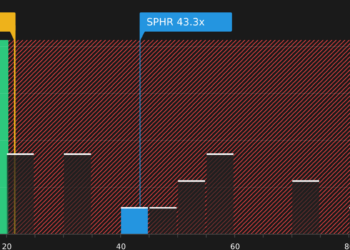

- Sphere Entertainment recently attracted attention after Zacks assigned it a Momentum Style Score of A and a Zacks Rank of #2 (Buy), reflecting improved analyst sentiment and positive earnings estimate revisions in the period leading up to today.

- This shift in sentiment highlights how changing expectations for Sphere’s earnings power and momentum profile can influence how investors view its longer-term prospects.

- Next, we’ll examine how this stronger earnings momentum, highlighted by upgraded estimates, may influence Sphere Entertainment’s existing investment narrative and risks.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

Sphere Entertainment Investment Narrative Recap

To own Sphere Entertainment, you need to believe its immersive-venue model can translate strong recent momentum into durable cash generation, despite high costs and execution complexity. The upgraded Zacks Rank and Momentum Score highlight improved earnings expectations, but they do not materially change the near term catalyst, which still centers on sustaining profitable operations at the Las Vegas Sphere. The biggest risk remains that high fixed costs outpace attendance and sponsorship revenue if demand proves less durable than hoped.

Among recent developments, Sphere’s addition to multiple S&P indices in March 2026 is most relevant to this momentum-focused news. Index inclusion can support liquidity and raise the company’s profile with institutional investors at a time when its Q4 2025 results showed full year revenue of US$1,220.05 million and a modest profit, reinforcing the near term narrative around earnings quality, but also putting more scrutiny on whether that profitability can be maintained as growth normalizes.

Yet behind this momentum, investors should be aware that rising maintenance and upgrade costs for Sphere’s complex venues could…

Read the full narrative on Sphere Entertainment (it’s free!)

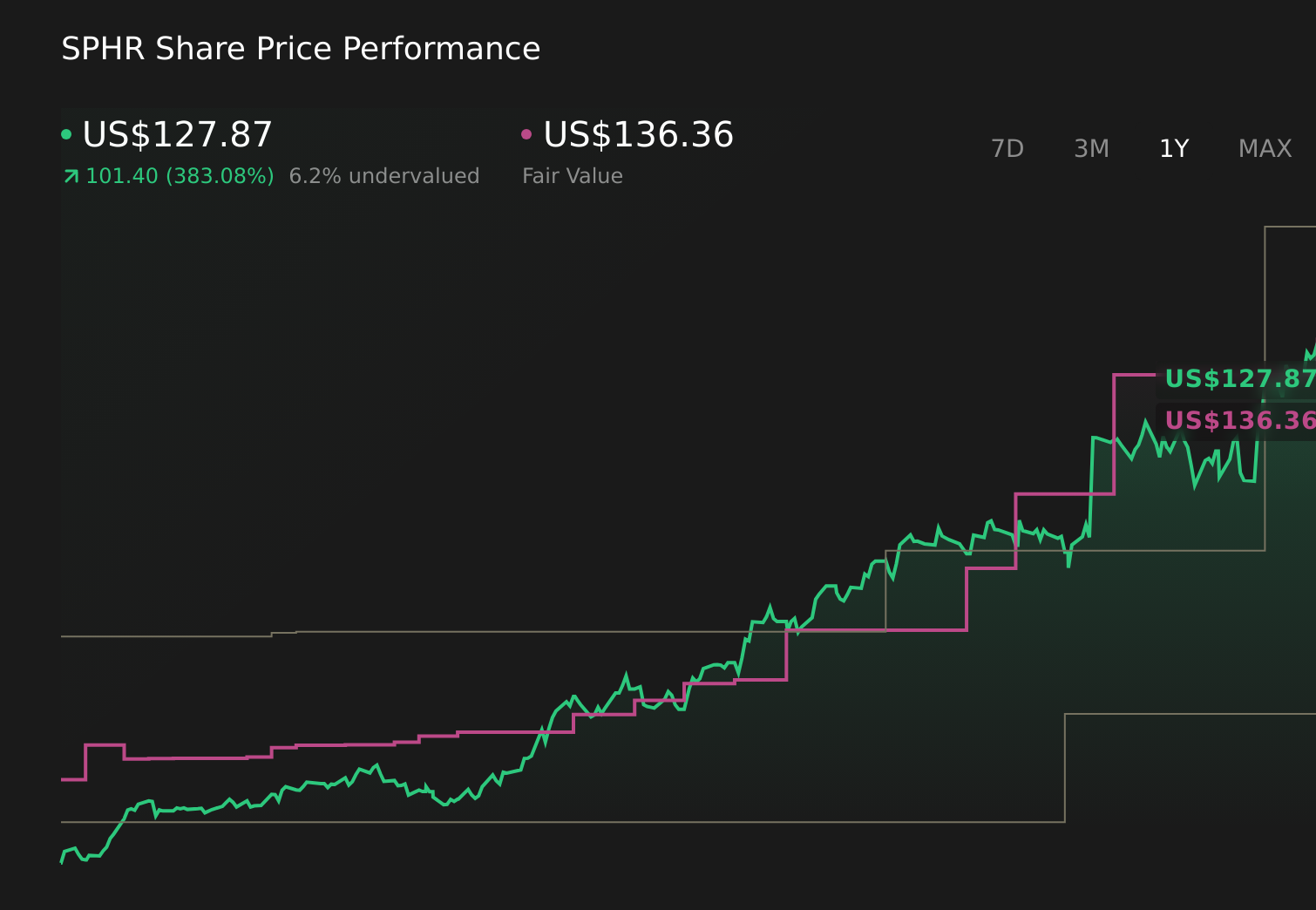

Sphere Entertainment’s narrative projects $1.3 billion revenue and $128.8 million earnings by 2029. This requires 2.5% yearly revenue growth and about a $95 million earnings increase from $33.4 million today.

Uncover how Sphere Entertainment’s forecasts yield a $136.36 fair value, a 7% upside to its current price.

Exploring Other Perspectives

While consensus focuses on near term profitability swings, the most optimistic analysts see Sphere’s long term upside in a global venue and content network, with revenue reaching about US$1.4 billion and earnings about US$148.5 million in their pre news 2029 view. In contrast to concerns about high capital intensity, they treat expansion as a key growth engine, which today’s momentum driven sentiment shift might either reinforce or challenge as new information emerges.

Explore 2 other fair value estimates on Sphere Entertainment – why the stock might be worth just $136.36!

Form Your Own Verdict

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’