Sphere Entertainment has delivered very strong share price gains over the last three years, yet the valuation signals are pulling in different directions, with the Discounted Cash Flow (DCF) intrinsic value estimate pointing to some upside while market based multiples look stretched.

- Sphere Entertainment has returned roughly 387.2% over three years, which puts a spotlight on whether recent gains already reflect most of the good news in the story.

- Expectations around demand for The Wizard of Oz at Sphere may support growth assumptions in the intrinsic value work. However, any disappointment in show performance or broader earnings could weigh heavily on what investors are currently willing to pay.

- On the broader valuation checks, Sphere Entertainment screens as undervalued on only 1 of 6 measures, which leans more toward an expensive stock than a clear bargain.

The issue now is whether Sphere Entertainment’s strong run and mixed valuation signals still leave enough room for a margin of safety at today’s price.

Is Sphere Entertainment a Bargain on Cash Flow?

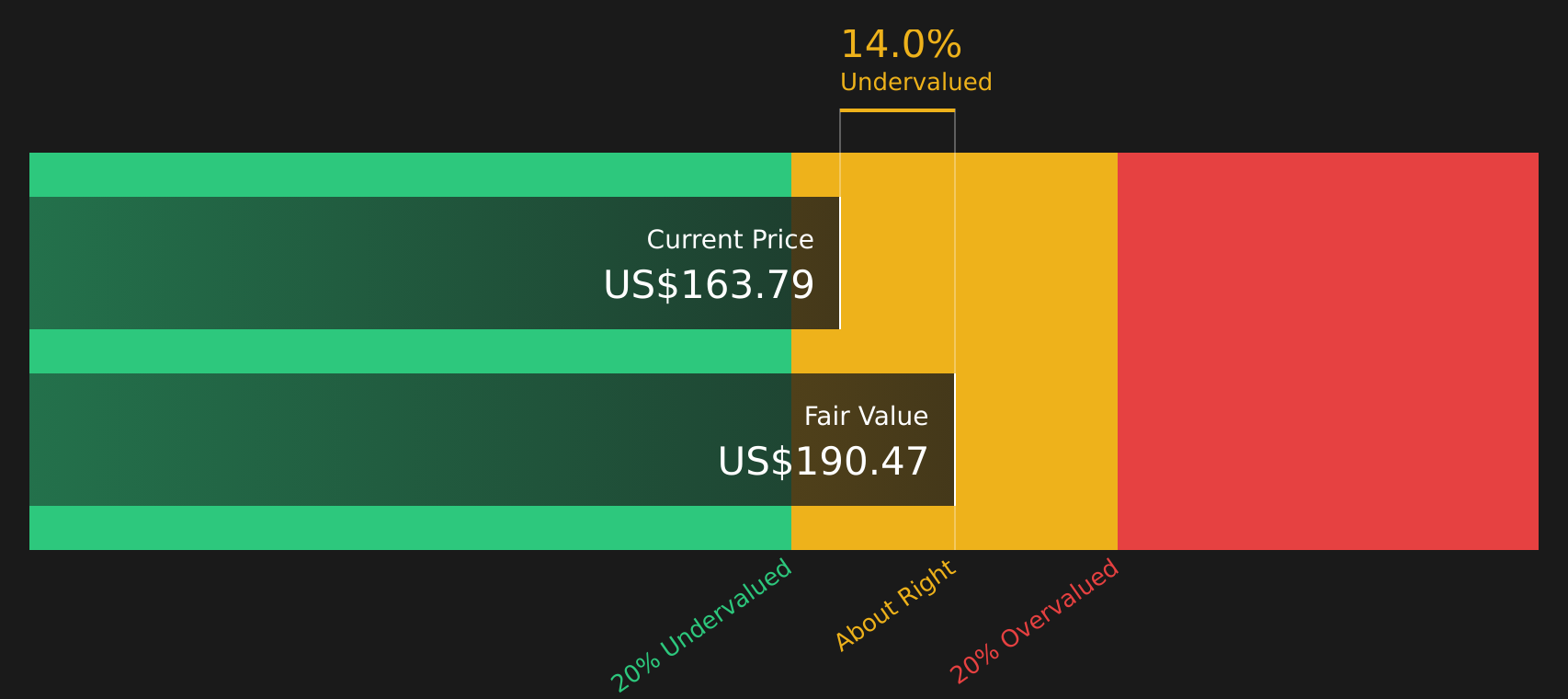

The Discounted Cash Flow (DCF) model values Sphere Entertainment by projecting its future cash generation and discounting it back to today. Sphere Entertainment currently reports latest twelve month free cash flow of about $84.6 million, and the model assumes growing cash flows over time rather than a flat or shrinking profile.

On these assumptions, the DCF model points to an estimated intrinsic value of about $190 per share, which implies the stock trades at roughly a 14.0% discount to that cash flow based value. Because expectations for The Wizard of Oz at Sphere are a key driver of those growth assumptions, any shortfall in show driven free cash flow would weaken the support for this intrinsic value.

Because recent analyst enthusiasm around Sphere Entertainment and The Wizard of Oz coincides with the shares still sitting below the DCF estimate, the cash flow work suggests the optimism has not yet fully closed the gap. The DCF outcome indicates Sphere Entertainment stock currently appears undervalued relative to its projected cash flows.

Our Discounted Cash Flow (DCF) analysis suggests Sphere Entertainment is undervalued by 14.0%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Sphere Entertainment Getting Expensive on Earnings?

The P/E ratio is a useful yardstick for Sphere Entertainment because earnings are a key focus for entertainment stocks with large venue and content investments. Sphere Entertainment currently trades on a P/E of about 51.5x, compared with an Entertainment industry average of roughly 23.0x and a peer average around 35.2x, so the stock is priced at a substantial premium to both its sector and direct peers.

The internal model that blends factors such as Sphere Entertainment’s growth profile, margins, size and risk points to a fair P/E closer to 3.6x. That figure is extremely low relative to the current 51.5x, which indicates the framework is heavily penalising the company, but it still suggests that the stock screens as expensive on an earnings basis rather than offering a comfortable entry point.

On the P/E multiple, Sphere Entertainment appears overvalued, with the market paying a high price for each dollar of current earnings.

See what the numbers say about this price — find out in our valuation breakdown.

The Sphere Entertainment Narrative: What Would Justify Today’s Price?

For Sphere Entertainment, Simply Wall St Narratives sit between the mixed valuation signals and your own judgment by spelling out which specific paths for growth, margins and earnings would need to play out for the stock to be worth meaningfully more or less than it is today, and they sit on Simply Wall St’s Community page. Instead of giving just one headline valuation figure, Narratives unpack the future it relies on so you can watch how those assumptions hold up over time.

Sphere Entertainment splits the community, with one camp focused on scalable IP and venues and the other worried about the cost and demand risks behind that story.

Bull case: roughly fairly valued

“Monetization of proprietary Sphere Studios technology and content such as AI-driven immersive productions across a global network of venues unlocks incremental, high-margin earnings streams and reinforces Sphere’s competitive moat beyond traditional ticket sales…”

Read the full Bull Case to see why Sphere Entertainment could be undervalued

Bear case: 184% overvalued

“The company’s strategy involves massive upfront capital expenditures for new venues and proprietary content, creating long-term fixed cost burdens; with even a moderate dip in demand or underperformance of blockbuster content, these obligations will drive persistent margin compression and leave net earnings highly vulnerable…”

Read the full Bear Case to see why Sphere Entertainment could be overvalued

Do you think there’s more to the story for Sphere Entertainment? Head over to our Community to see what others are saying!

The Bottom Line

Sphere Entertainment sits in a genuine tug of war between the Discounted Cash Flow (DCF) intrinsic value estimate, which points to a 14.0% discount, and market multiples that flag the stock as overvalued. The gap is largely about timing and risk, with the DCF leaning on future cash generation while the high P/E reflects elevated expectations and a penalty for execution and funding risks. Broader valuation checks remain weak despite the DCF support. The key question is whether demand and margins around Sphere’s venue and content pipeline, especially The Wizard of Oz, can deliver enough durable cash flow to justify both the current price and the premium earnings multiple.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

‘ The preceding article may include information circulated by third parties ’

‘ Some details of this article were extracted from the following source simplywall.st ’